March 2019

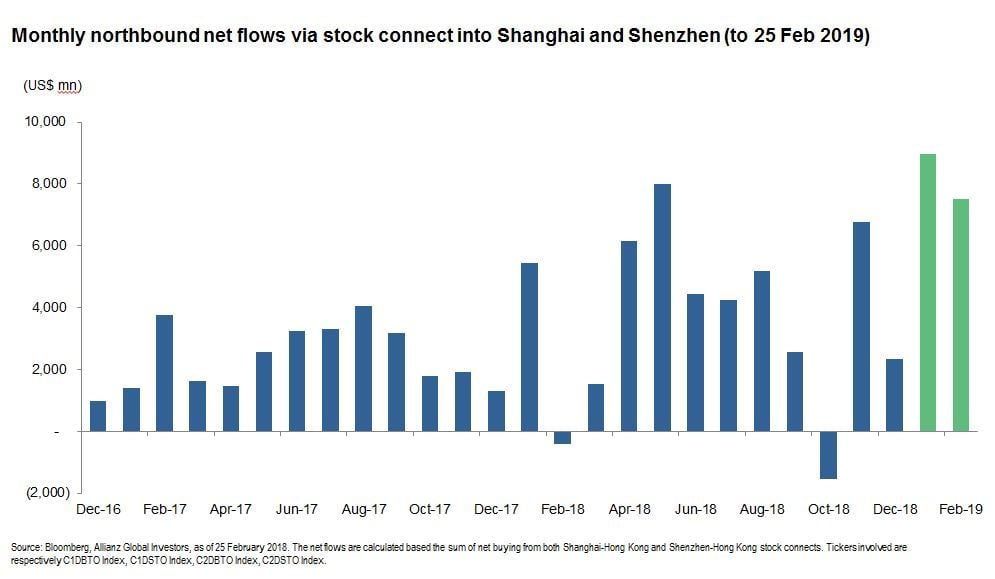

MSCI has announced that it will significantly increase the weighting of China A-shares – the world’s second largest equity market after the US - in its widely-followed indices. This news was expected as the muted market response shows. However, the implementation of the inclusion will happen more quickly than anticipated. It will take place in three stages this year in May, August and November. Previously, May 2020 was the expected timeline for completion of this stage. China A-share mid caps will also be included from November 2019. As a result, the weighting of A-shares will increase from 0.8% to 3.3% in the MSCI EM Index. Of course to an extent, the heavy foreign buying this year (over USD 16bn in January and February through Stock Connect – see chart on the next page) was in anticipation of this announcement. However, it is estimated that close to half of EM funds do not currently have China A-shares exposure. Being underweight by 0.8%, however, is a very different consideration to being underweight by 3.3%, and therefore this news is likely to prompt a significant shift in attitudes towards the market. In aggregate, the change is expected to result in a potential inflow of around USD 70bn – not large in the context of Shanghai and Shenzhen daily market turnover (sometimes over USD 100bn), but the further growth of an institutional shareholder base will continue to improve the market structure. Indeed, the explanation for this move is based on advancements in accessibility issues, an acceleration in the pace of market opening, and an improvement in the regulatory structure evidenced by a significant reduction in the number of stocks with trading suspensions. This endorsement from a reputable institution such as MSCI will add further credibility to the asset class.

This poses a challenge to global investors – continue to get exposure to China through EM strategies and gradually increase exposure as the benchmark weightings increase. Or build a separate and dedicated exposure to China either through a China A-share allocation or through an ‘All China’ approach and thereby pre-empt the index moves.

The news, in our view, increases the likelihood that more investors will opt for specialist China A-share managers to complement EM positioning.