March 2019

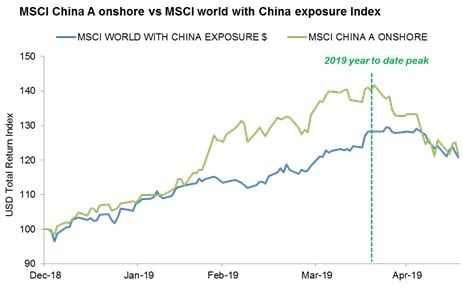

Not surprisingly China A-shares – as a volatile and sentiment-driven market - has experienced some of the weaker performance recently. The market is down around 14% from the mid-April 2019 peak. This is compared to a 6.8% correction in the MSCI World with China exposure index (see chart below).

The MSCI World With China Exposure Index comprises 51 global stocks with the highest revenue exposure to China. Constituents include Qualcomm and Broadcom, where 67% and 49% of revenues in 2018 were derived from China respectively.

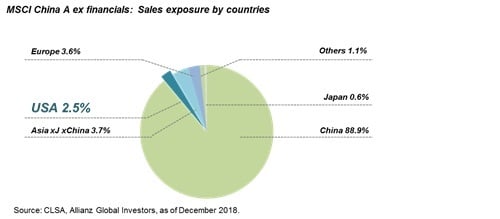

In theory, these companies stand to suffer most in a US-China trade conflict, even more so potentially than China A-shares companies, where in aggregate only 2.5% of ex-financials revenue is derived directly from the US. This is a reminder that China A markets are volatile and fluctuate much more than economic fundamentals as a result of the underlying nature of the shareholder base.

The extent of the market decline in China A-shares in recent weeks to a large extent reflects the strength of the market recovery year to date. At one stage China A shares had rallied by more than 40%. The question now is does this trade conflict escalation signal a return to the 2018 bear market in China? We think it is unlikely and view the pullback as a healthy and much-needed correction. A key reason is that the economic situation in China now is different to last year. A combination of monetary and fiscal policy easing has resulted in a more stable environment, compared to the focus on deleveraging policies in 2018 which created a credit squeeze and a period of bumpy economic deceleration. Evidence of the fundamental position now is the net profit growth for listed Chinese companies (across A, H, and US listed ADRs) which rebounded to 11% YoY in Q1 2019. Street consensus for 2019 full year earnings growth is still double digit for both onshore and offshore Chinese equities. While these figures look, as usual, overly optimistic, they signal a more encouraging longer term outlook.

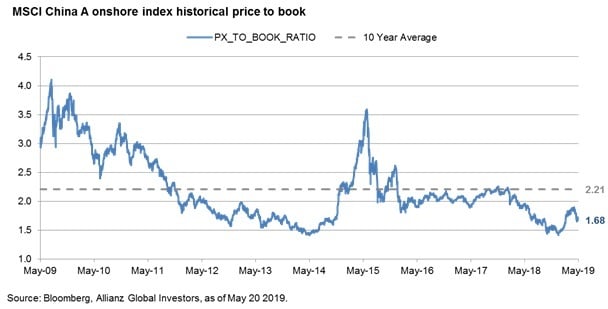

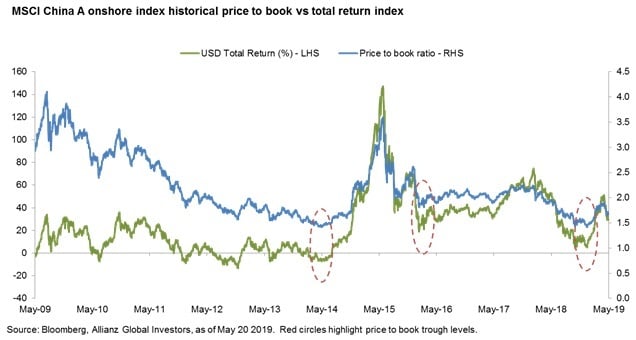

With earnings being resilient, the market pullback has effectively come about as a result of lower valuations. The forward price/earnings ratio for MSCI China A-shares Onshore Index is 11.3x, compared to the 10 year average of 13.2x. The price/book ratio of MSCI China A-shares now stands at 1.68x, meaningfully lower than the 10 year average of 2.2x. Historically these sorts of valuations have signaled a good entry point for longer term investors, as shown in the charts below.

There have been no changes to the inclusion schedule announced by MSCI. This means that the weight of China A-shares in its EM index will double on May 28, 2019. 26 new China A-shares stocks will be added and the inclusion factor will increase from 5% to 10%. China A-shares will account for 1.76% of MSCI Emerging Market Index at the end of May 2019. As planned, the inclusion factor will further rise to 20% in November 2019, by which time China A-shares should account for 3.3% in MSCI Emerging Market Index. This is still just the beginning of a much longer term story. As suggested by the pro-forma analysis below, China A-shares have the potential to ultimately become close to 30% of MSCI Emerging Market Index.

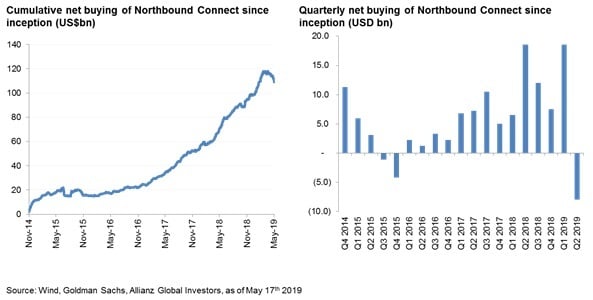

Our answer is not really. According to the latest analysis by Goldman Sachs, global EM managers have an average of 2.4% exposure to China A-shares as at April 2019, still behind the year-end target weighting of 3.3% in MSCI EM Index. We can see in Northbound stock connect flows, there has been some selling recently after the strength of the recent rally (see charts below), but the extent is significantly less than that of previous inflows.

For those who made a 40% return in short order, some profit taking is not unexpected. However, given the structural underweight position of many investors, our view is these outflows are likely to be quite short lived, as we have seen in the past.

In terms of our China A-shares and All China portfolio positioning, we have been using the market pullback to add to favored holdings. Clearly some stocks with exports to the US have been impacted, but the share price weakness has generally been a lot greater than the earnings hit as a result of tariffs. The tendency of local investors to over-react to short term news flow should therefore hopefully be an opportunity for us to add value in the medium to longer term.