May 2019

In our view, there is a significant gap between perception and reality of China’s State-Owned Enterprises (SOEs). For some people, SOEs are dinosaurs—old-style companies that absorb resources from the economy but add little economic value. They have long been synonymous with low efficiency, questionable governance and poor shareholder returns.

The reality, however, is that the state owned system in China has gone through significant change over the past 40 years. And during this time, SOEs have both taken on different roles in the economy and are managed in very diverse ways. Generally the SOE sector is much smaller now than it used to be, but remains firmly in control in key strategic sectors. In this article, we hope to help clarify some of the misunderstandings about Chinese SOEs, not only through facts and figures, but also through our experience of interacting with these companies and the people behind them. We believe that in aggregate the SOE sector is now better managed and offers a wider opportunity set to investors. But being selective is essential.

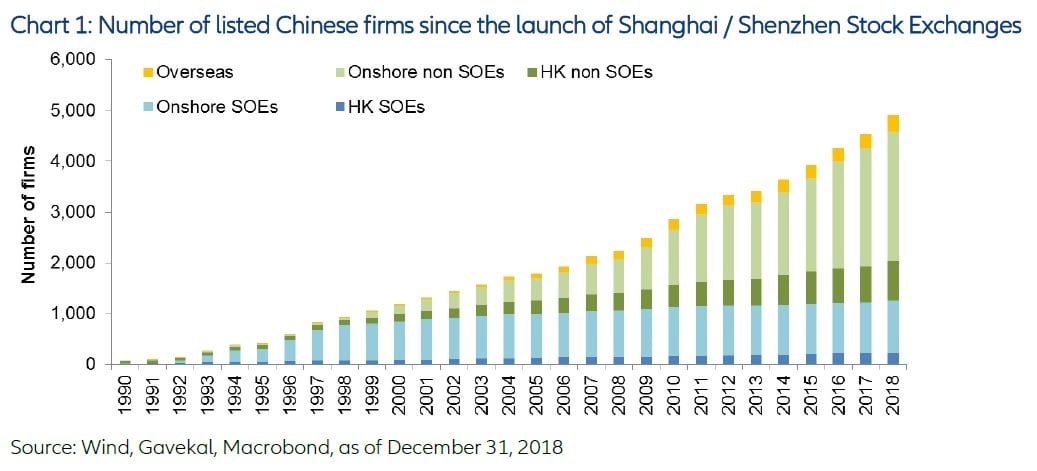

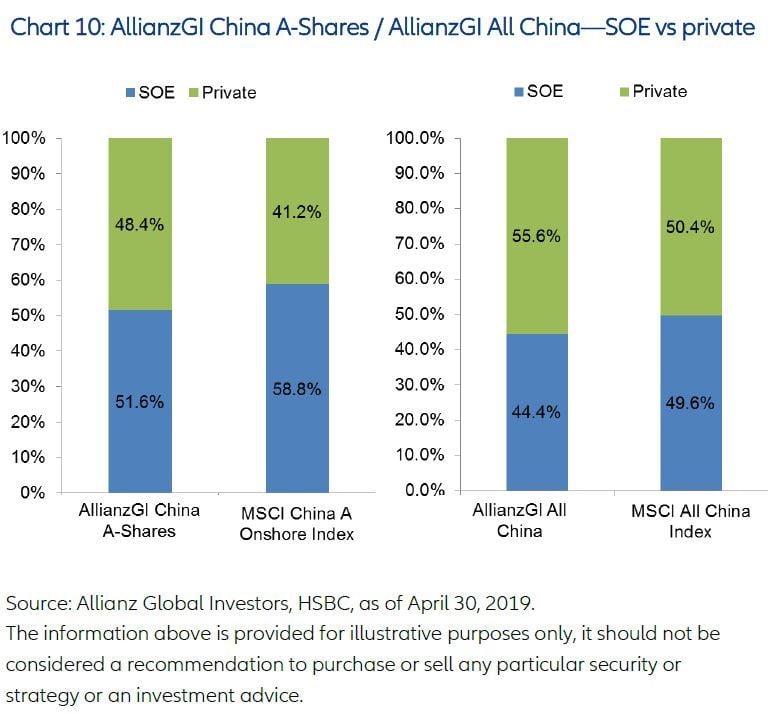

Since economic reform and opening-up policies began in 1978, China’s SOEs have undergone a long process of gradual and progressive transformation. Today, SOEs are a slimmed down version of their former selves. The number of enterprises, assets and employees has shrunk over the years - the SOE share of GDP has fallen from more than 50% to less than 30% over the past 15 year. In 2003, SOEs accounted for 18% of all industrial enterprises, now this figure has fallen to 5%1. 1. Source: HSBC, SOE reform in China, as of November 2018. This change has also been reflected in stock markets, where their overwhelming dominance started to decline as private sector IPOs accelerated in the late 1990s. Today there are far more private companies than SOEs within the Chinese listed equity universe, although SOEs still account for around half of the overall market capitalization.

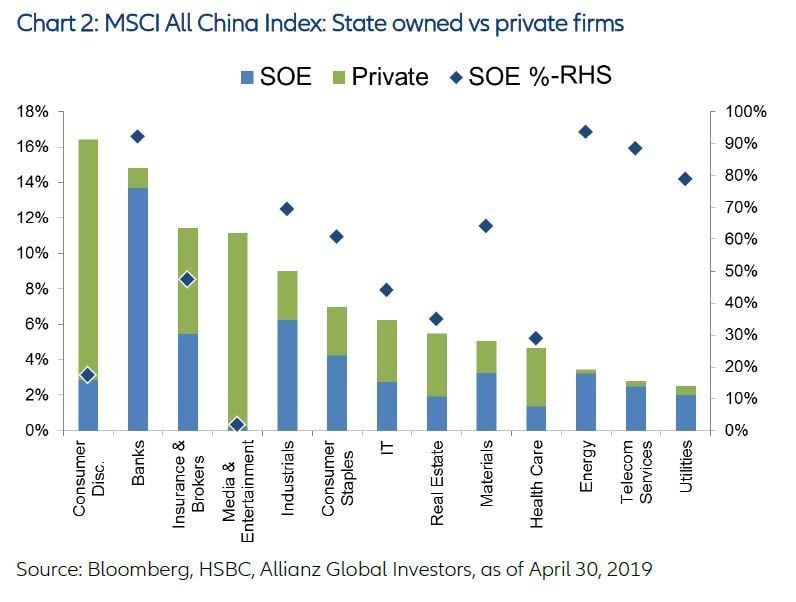

Albeit a smaller size overall, state-owned companies still dominate the strategic industries in China. As shown in the chart below, SOEs represent over 80% of the investment universe in banks, energy, telecoms and utilities (Chart 2). Put simply, the supply and prices of production factors such as bank loans, oil, electricity and the telecom networks are still mostly state controlled, hence SOEs remain highly influential within China’s economy.

In China, ‘SOE reform’ is very different from the concept of privatization. Compared to the “shock therapy” where radical economic liberalization is encouraged, SOE reforms in China are usually incremental and pragmatic, in the sense they are implemented with a view to the country’s long term economic goals. The best way to interpret China’s SOE reform policies is to understand the role that SOEs are expected to play from policymakers’ perspective. SOEs should take the lead in advancing national policy goals, especially technological self-reliance and global influence. SOEs are also expected to take on the responsibility of “national service”, i.e. providing public goods, supporting employment and stabilizing the economy / market when necessary. Parallel to these is the goal of sustainable profit growth and enhancement of competitiveness, which is also a key focus of SOE reform measures.

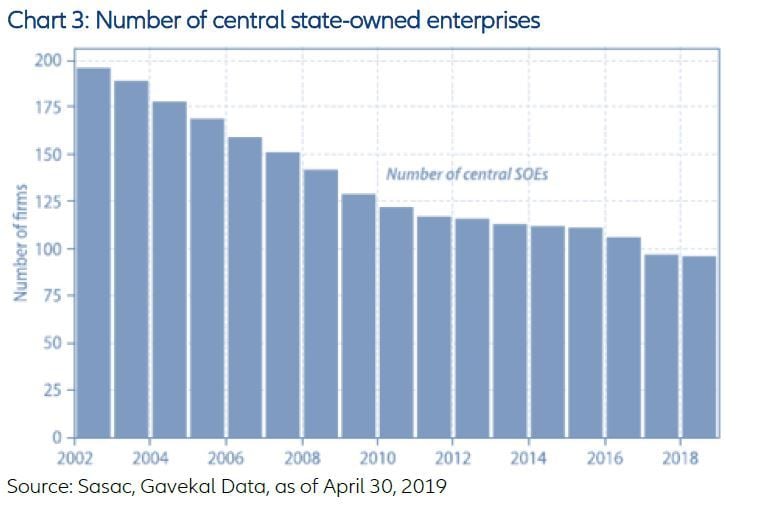

The first category is SOEs in strategically important industries, including energy, transportation, and even semiconductors. In these areas, the state’s ability to control and mobilize resources is considered key to help Chinese players achieve global competitiveness. What we have seen in this area is significant consolidation, so that already-large SOEs have become even bigger in order to compete internationally. In 2015 for example, train manufacturers CSR and China CNR were merged to help focus on beating foreign rivals instead of competing against each other. As a result of the overall consolidation, the number of central SOEs has fallen from close to 200 in 2002 to 97 currently2. 2. Source: CCTV, as of April 5, 2019.

Of course bigger has not always been better, at least from an investor perspective. While merged enterprises should in theory benefit from economies of scale, the synergies through consolidation and cost reduction processes has often disappointed. In some material sectors such as cement, glass and steel production we have seen the closure of excess production capacity which has helped to stabilize prices and therefore profitability. But in many other cases, the national service requirements of SOEs to provide employment and contribute to social stability—combined with a lack of incentive for senior management to make tough decisions—have prevented more radical restructuring.

The second category refers to SOEs in non-strategically important industries, such as consumer products & services, healthcare, construction machinery, etc. SOEs in these areas have a much greater market-orientation, and share a more level playing field with private companies.

Successful SOEs in these areas often share some common traits: a workforce incentivised through employee stock ownership plans, professional managers with strong industry background, introduction of independent board members, well-established distribution networks and brand names accumulated over the years, and finally limited state influence or even a helpful private partner through mixed ownership reform.

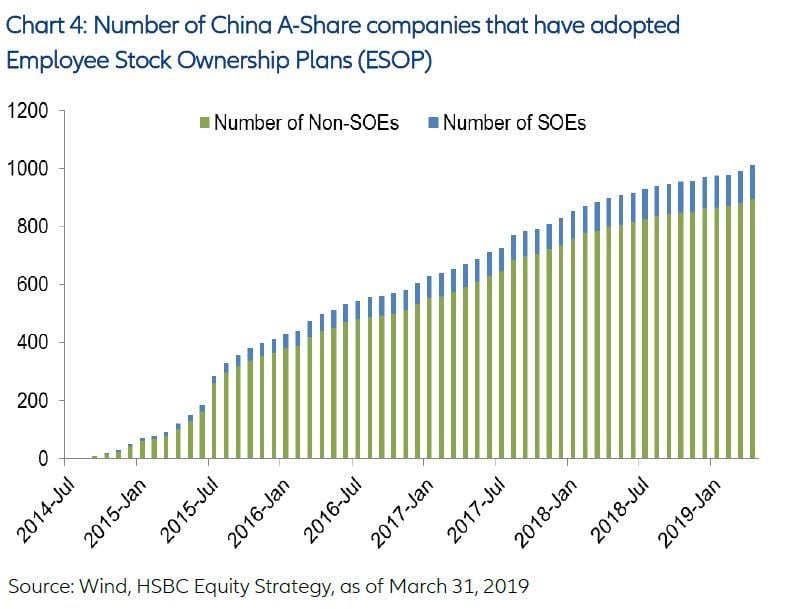

During our research process, we spend a significant amount of our time in understanding the people behind the business, especially the incentive structures for SOE managers. It is encouraging to see a rising number of SOEs adopting employee stock ownership plans (ESOPs), which help to better align management interest with that of minority shareholders.

Of course, an ESOP is not a magic solution that works in every case; however, properly designed and structured, it can be an important indicator and a reflection of corporate governance and business culture.

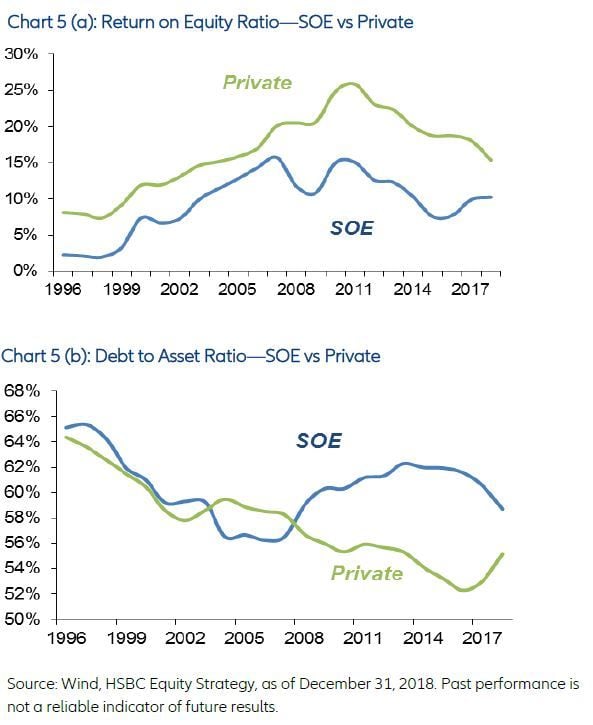

Over the past 5 years, we have seen a recovery in SOE profit growth and a drop in leverage among SOEs, closing the gap versus privately owned companies. Apart from the impact of SOE reform, the recovery in commodity prices also helped boost margins especially for SOEs operating in upstream industries.

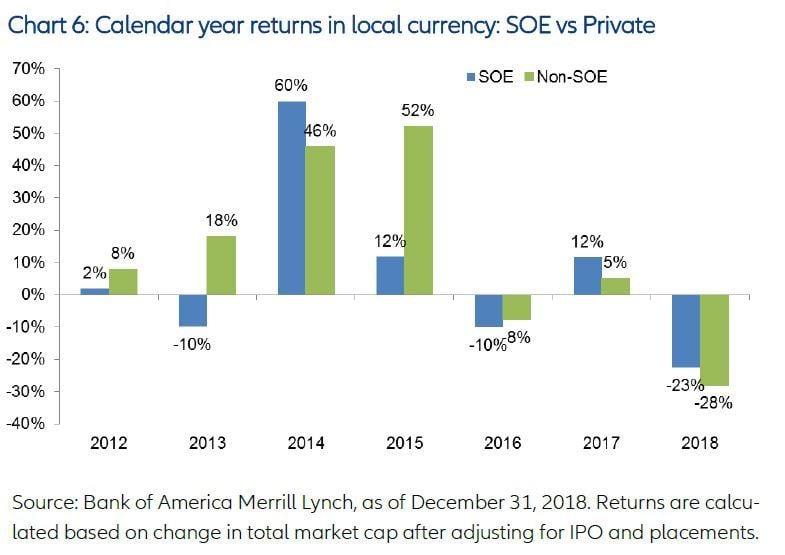

If we examine the equity market performance of SOE stocks vs their private counterparts, there is no consistent pattern. Indeed SOEs have outperformed in 3 of the last 7 calendar years and 2 of the last 3. This suggests that not all SOEs are necessarily bad investments. Our own experience has been that certain SOEs have traded on discounted valuations because of the ‘SOE label’, which fails to take into account the future benefits of the reform program.

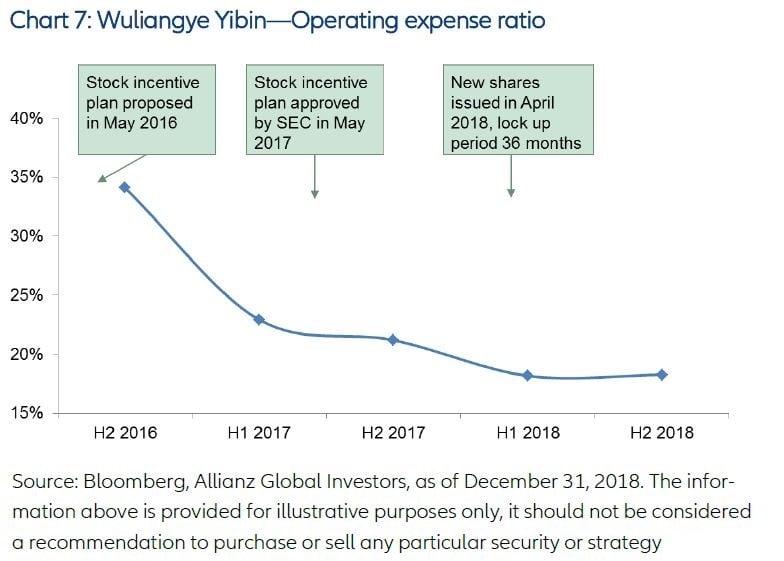

A case in point is a local government owned SOE called Wuliangye Yibin (WLY), one of the top ten holdings within AllianzGI China A-Shares strategy. This is China’s second largest producer of “white liquor”, the national drink of China. White liquor is drunk almost exclusively at meals and used during toasts to show respect and build relationships.

In May 2016, WLY introduced an employee stock ownership scheme based on profit targets to both top and middle management3. Since then we have seen management making significant efforts to enhance productivity, reflected in a reduction in operational expense ratio from 34% in H2 2016 to 18% in 2018. There has also been a notable cultural change in the way the company has become more transparent and market oriented when communicating with shareholders.

3. Source: World Bank Database, as of December 31, 2015.

We generally find more investment opportunities in the non-strategic SOE areas. In the strategic SOE space, although the reform progress has generally seen slower, there are still some companies that stand out. For example, one of the top ten holdings within AllianzGI China A-Shares strategy has been China Merchants Bank (CMB), a nationwide bank controlled by state-background China Merchants Group. This bank differentiates itself with clear business strategies to focus on retail banking and SME clients, and has over time established a strong brand name, a business-oriented management team and a highly experienced banker network which are difficult for competitors to replicate.

In terms of management, it is notable that the CEO is one of the few overseas educated leaders within the Chinese banking industry. Compared to the average 2 – 3 year tenure of top management in the big four state banks, the CEO of CMB has been in his position since 2013, a key reason behind the consistent execution of the business strategy. Over the past 5 years, CMB delivered stronger than peers earnings growth and higher return on equity ratio.

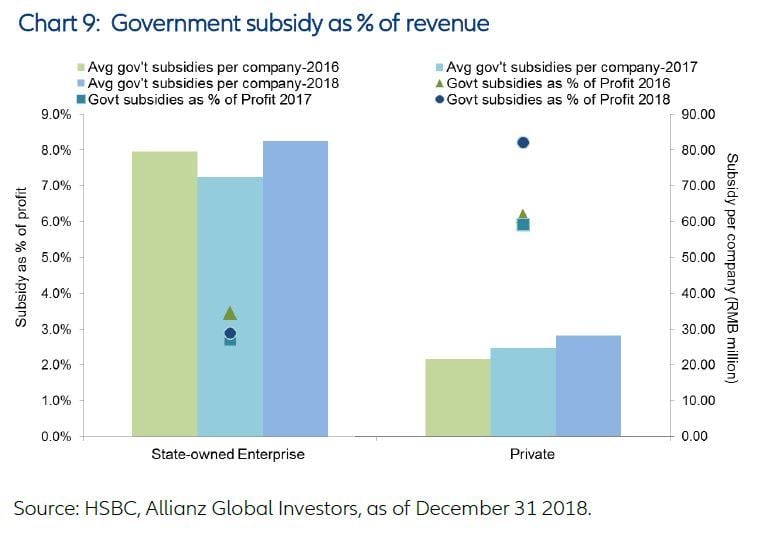

Despite the success stories mentioned above, as a rule SOEs are managed to service the nation or advance long term strategic goals, which tend to conflict with minority shareholder interests. For example, SOEs can be treated as convenient growth stabilizers. The post global financial crisis fiscal stimulus and credit expansion was one of the main reasons for the sharp increase in SOE leverage a decade ago. And when it comes to China’s international ambitions, such as the Belt and Road initiative, state owned construction companies are typically the first movers into overseas markets, being forced to accept an unpalatable mix of lower margins and higher geopolitical / execution risk. Another commonly cited risk is the dependence of SOEs on government support, such as preferred policy treatment and subsidies. On average, listed SOEs in the A share markets received RMB 82.6 mn (USD 12m) of subsidies in 2018, which is significantly higher than their private peers (see Chart 9). Heavy industry, utilities, materials and auto companies are the biggest recipients of this support. But as a percentage of profits, the subsidies received by private companies is in aggregate higher than that of SOEs.

The key takeaway is the perception that SOEs are generally zombie companies surviving only because of government support is wrong. Clearly there are some that are subsidy and policy-dependent, but many others have become significantly more market-oriented over time.

There is no magic formula to help us navigate the SOE risks. The key is to understand the people behind the business, their aspirations and incentives, as well as execution capability. This requires on-the-ground work to engage with management, cross check along the supply chain, and using our Grassroots® Research network to verify our research.

Despite all the skepticism over state owned enterprise reforms in China, a lot of progress has been achieved in recent years. Overcapacity has been slashed across a range of industries, debt burdens are easing, and stock incentive schemes for management and employees are becoming more popular. Of course there is still a long way to go and there are still many SOEs that face challenges including low-efficiency and questionable governance. Nonetheless, the perception that SOEs are old-style companies that add little economic value is misguided and can lead to valuation anomalies in the equity markets.