August 2019

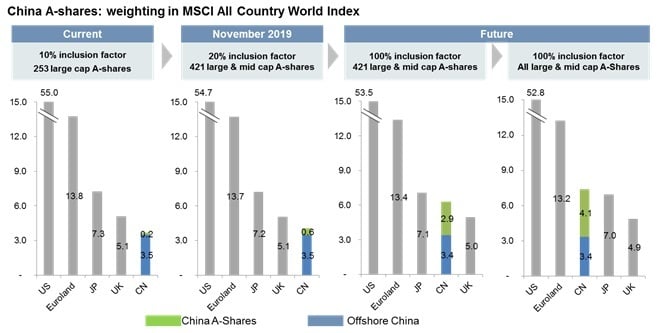

According to the plan, this MSCI China A-Shares inclusion will be implemented via three steps:

Now we are progressing well into the second step. By end of November 2019, China A will become ~3% of MSCI EM Index and ~10% of MSCI China Index.

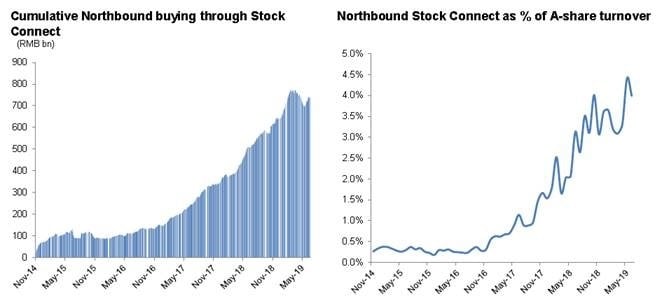

While the inclusion plan is well known, the announcement reflects the continuous acceleration of A-Shares internationalization, despite of the ongoing dispute over trade, tech and currency between US and China. In addition to MSCI, FTSE Russell and S&P Dow Jones also plan to include China A-Shares this year. It is estimated that the rising China A-Shares representation with global indices would bring Rmb300-400bn (USD 43 – 57 bn) passive fund inflow to China A in 2019. At the same time, some active foreign investors that buy into the China A-Shares story have been taking advantage of the market volatility to build their position ahead of benchmark changes. In the first half of 2019, there has been RMB 97 bn (~USD 14 bn) cumulative flows into China A-Shares through stock connect channel. However, given the significant market size, northbound foreign investors only represent ~4% of total market turnover within China A-Shares.

Our answer is yes. The underpinning factor behind the structural inflow into China A-Shares is increasing representation of China A-Shares within global indices and the continuous opening up of China’s capital market. Ultimately, we believe China A-Shares has the potential to become 20%+ within the emerging market index, which means China overall (A-Shares + offshore) could represent 40 – 50% of the MSCI Emerging Market Index. By that time, China will surpass Japan as the third largest market within MSCI All Country World Index, just after the US and Europe (see chart below). This means, China will become a stand alone asset class.

The natural next step for investors is to decide how to allocate to China. For investors with existing emerging market exposure, adding a pure China A-Share allocation has the benefit of complementing EM strategies without duplicating offshore China exposure. Historical return analysis shows that adding China A on top of an typical EM portfolio could have helped enhance risk / return profile. For investors who do not want to make an onshore China vs offshore China asset allocation decision, we believe a holistic, “All China” approach investing across all Chinese equity markets would make sense.