December 2019

2019 marked the 70th anniversary of the People’s Republic of China. And it has certainly been an eventful year. Geo-politics have taken center stage with the escalation of the off-again, on-again China-US trade war. This extended into a technology conflict, with the Hong Kong protests adding further complications. And from an economic perspective it was a year of further deceleration in China, albeit more consistent and better managed compared to the bumpy journey of 2018. If we had used our crystal ball to accurately forecast all these macro headwinds, the presumption would probably have been a tough equity market environment. But, to the contrary, it has been a year of strong performance. The MSCI China Index is up 20.0% and MSCI China A Onshore index up 33.6% year-to-date (as of December 16 2019, USD total return). Both onshore and offshore markets have clearly become more resilient to external shocks. Perhaps investors have adjusted to what increasingly looks like ‘the new normal’ of heightened and ongoing geopolitical conflict. And so to the year ahead. Looking at the China A market as a whole, the valuation is around 12x forward PE. This compares to expected earnings growth of 8% - 10%.1 Both relative to earnings and in a historical context, valuations therefore look reasonable. This is perhaps not surprising given that the market total return over the last 5 years is close to zero. From a beta perspective we are, therefore, reasonably optimistic about the outlook, particularly as we expect ongoing inflows from global investors. The MSCI journey to increase China A index weightings still has a lot further to go.

Source: Bloomberg, Allianz Global Investors, as of December 20, 2019.

Of course the China A story for the last 5 years has been all about alpha. Looking ahead, we see a number of promising areas. Below we highlight what we see as some of the key investment trends for 2020.

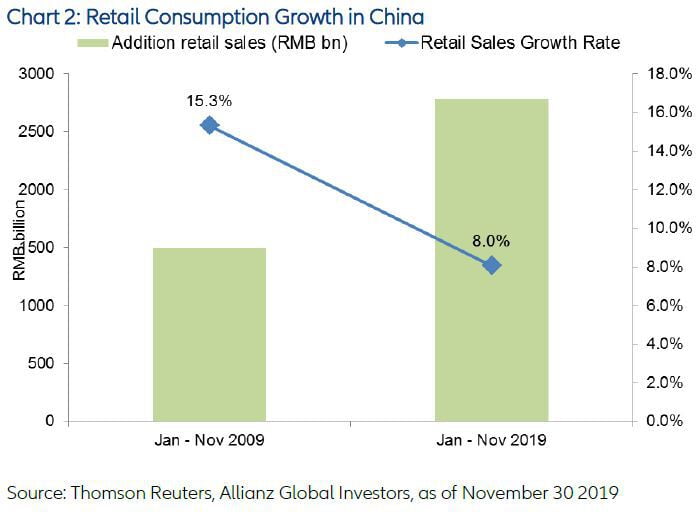

The consumer upgrade story in China is not new, but the scale continues to grow. The dollar value of total retail sales in China is now around 90% of the US level. Despite the slowing year on year growth, the scale is still impressive. In the first three quarters of 2019 alone, we saw an incremental RMB 2.8 trillion (~USD 400 bn) retail sales in China. And Alibaba set a new Singles Day record in 2019 with over USD 30 billion of sales, the world’s largest 24 hour shopping event. In comparison, this is around 5x bigger than Black Friday in the US.

The sheer size of the economy, and increasing focus on premium products, creates both volume and margin opportunities for companies that can capture the change in consumption behavior, especially when combined with an innovative service model.

For example, within the general grocery business, eCommerce and modern retail channels such as hypermarkets and supermarkets will continue to gain share from traditional mom and pop stores formats, who are simply unable to match the scale and logistics required for effective distribution in China.

Technology is also playing a key role in the healthcare sector, where the fusion of science and computer processing speeds is resulting in new drug development, which would have seemed inconceivable a few years ago.

Combined with the naturally rising demand from an aging population, the healthcare sector should provide significant investment opportunities in the years ahead.

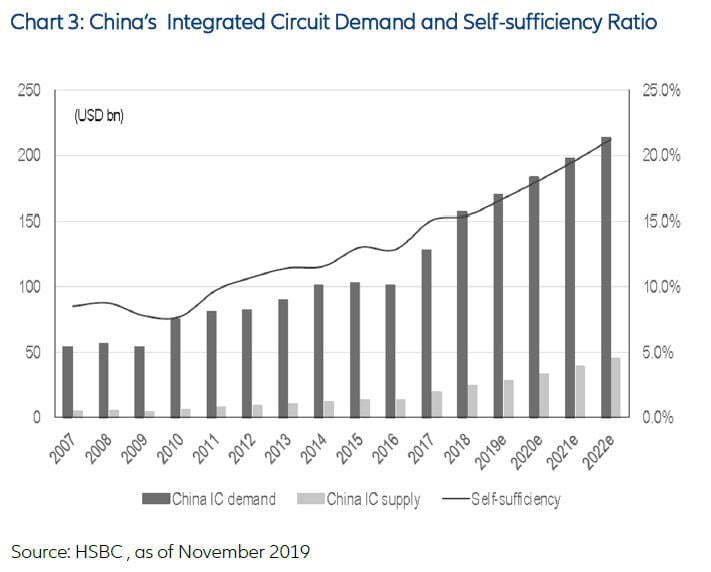

Since 2014, China has surpassed the European Union and become the second largest spender on research and development after the US. The escalation of the US - China trade conflict has served to accelerate R&D in China, especially in areas where the country has a strategic need for self-sufficiency.

In 2019, more than 100 Chinese entities were put on the US trade blacklist, which effectively cut off their access to American suppliers. Take semiconductors as an example.

China imported USD 312 billion of semiconductors in 2018, more than the value of imported crude oil. While the self-sufficiency ratio has been steadily on the rise, only around 15% of total semiconductor demand can be produced domestically. How to narrow the significant demand supply gap is a key challenge for the country, but will also create opportunities for domestic players with improving core technology.

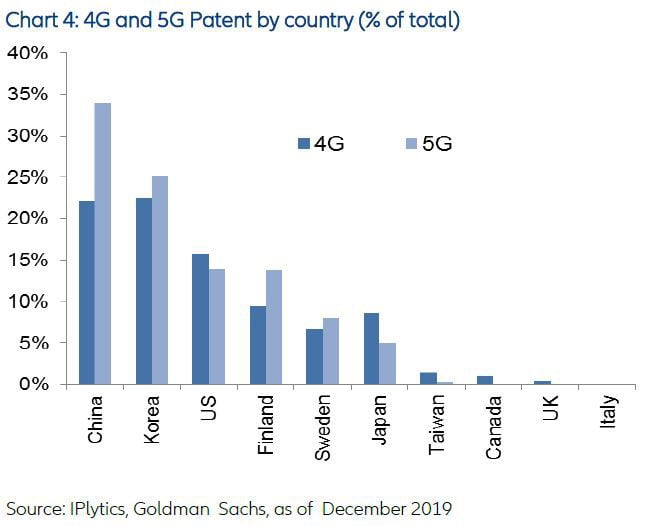

Elsewhere in the tech space, strong policy support and a large domestic market are proving to be tailwinds for the commercialisation of new technologies. Areas such as 5G infrastructure investment and the electric vehicle supply chain, especially upstream in battery equipment suppliers and new material companies, should see significant growth in the year ahead.

One of the features of A-Shares corporate behaviour in recent years has been a change of focus away from scale and towards more sustainable profit growth. Combined with many smaller companies finding it harder to get access to capital, this is also being reflected in a consolidation of market share, especially towards industry leaders with advanced technology, strong brands, and more effective management.

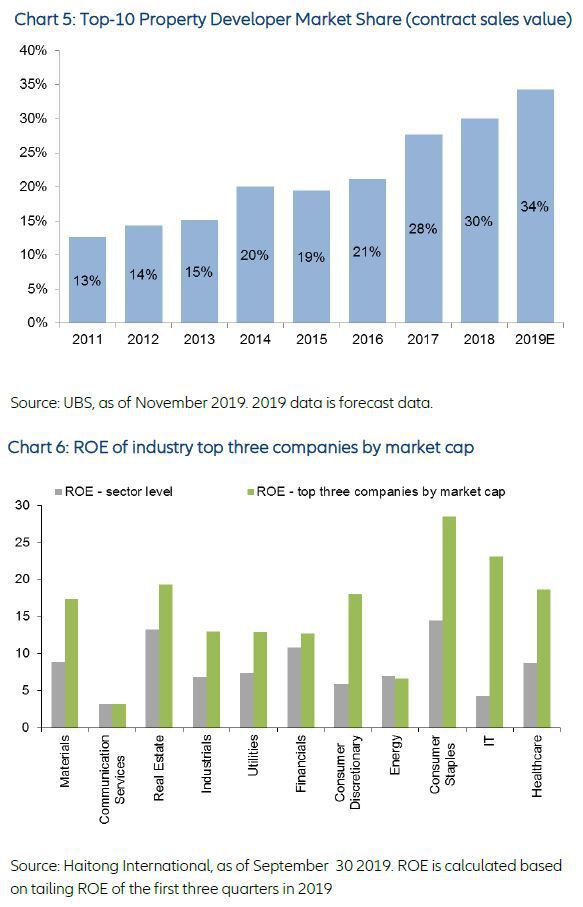

Industry consolidation has so far been more notable in more mature industries such as real estate. The top ten property developers in China, for example, have seen their market share grow from around 10% in 2011 to 34% in 2019 (Chart 5). Higher quality land banks, access to capital and professional project management capabilities have been key to their success.

As the economy continues to slow in 2020 - we would not be surprised to see a 5-handle on GDP forecasts - the trend towards industry consolidation is likely to become more widespread in other sectors. From an investment perspective, we generally view market consolidators as more likely to outgrow their peers and generate better shareholder returns, especially within niche industries.

Over the first 3 quarters of 2019, for example, data shows significantly higher ROEs from the top three industry leaders vs. their peers across most sectors.

In our view, it is unreasonable to expect a repeat of this large cap outperformance. The valuation anomaly that previously existed because many of these stocks were ignored by the local investor base, has to a large extent been corrected.

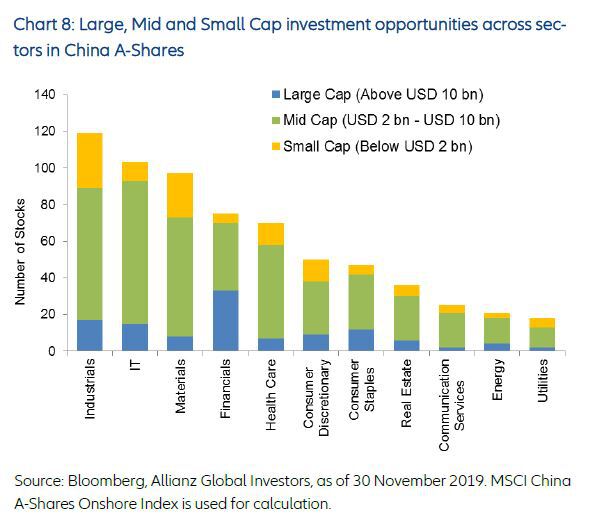

In contrast, we are finding more interesting opportunities in the mid and small cap space. Partly this is because smaller companies in China A-Shares are less well researched and therefore overlooked. In addition, expanding the investment universe also means getting exposure to opportunities in niche industries that enjoy secular growth potential, especially within IT, industrials and healthcare. It is also a particular characteristic of A-shares that the turnover of small and mid cap stocks is often much higher than large caps. This reflects the preference of onshore retail investors and means there is ample liquidity for institutional investors to participate in the mid and small cap space.

China equities, especially China A-Shares have been impressively resilient in 2019, in a challenging economic and geo-political environment. And we expect such uncertainties to continue into 2020. In terms of market performance, it is unlikely we will see the same level of market returns in 2020, especially given the re-rating that has benefited many large caps. Overall, however, we see a continuation of positive earnings momentum which should provide support to the market as a whole.

In recent years the alpha from China A-shares has been at least as important, if not more so, than the beta returns. And looking ahead we see a number of promising stock specific opportunities across a range of sectors and industries. Given that mid and small caps have lagged by 50% since the launch of the stock connect schemes, it is perhaps no surprise that we are finding more ideas in this area, as opposed to the large cap ‘foreign favourites’.