September 2018

It’s hard to keep track of all the trade-related headlines on China these days. The latest is the recent announcement of US tariffs on an additional USD 200 bn of Chinese exports, and subsequent retaliatory measures from China, which have again dampened investment sentiment. Of course, when the two largest economic powers which have contributed over half of global growth each year since 2002 and become increasingly inter-connected – Xi Jinping’s own daughter attended Harvard – come to blows, then investors will be understandably nervous. But in our view it’s too easy to blame this single factor when explaining why China equity markets have underperformed this year.

This is for illustrative purposes only, not a recommendation or solicitation to buy or sell any particular security. Past performance is not a reliable indicator of future results.

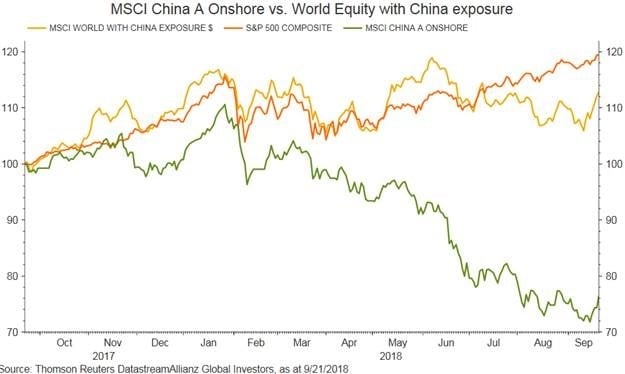

Take a look at the following chart. The yellow line is MSCI World with China exposure index, which consists of ~50 developed world stocks with the highest revenue exposure to China, and should in theory stand to be hurt the worst in a trade conflict between the US and China. Surprisingly these names have held up well and performed almost in line with the S&P 500 since the escalation of the trade conflict in March. Well-known stocks such as Nike (14.1% revenue exposure to China) and Apple (19.5% revenue exposure to China), for example, have gone up by around 25% since then. Meanwhile domestic China A-Shares (green line) have weakened significantly – even allowing for the recent 7% rally - despite the fact that China A-Share listed companies derive 88% of their revenue from domestic markets.

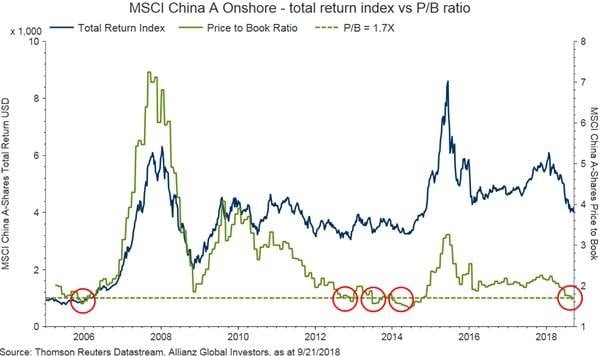

Another explanation – which is what most China A-Share companies tell us they are far more concerned about – is the impact of the China government’s ongoing deleveraging efforts, both in terms of slowing economic growth and also access to credit. The extent of the deleveraging process in the face of the external trade pressures has been surprising, and suggests the authorities in China may have been taken by surprise by US policy. Recent signals suggest a number of monetary and fiscal measures to help stabilize the economic situation in China – and more can be expected if the US further ratchets up the rhetoric. Where does this leave us on valuations? The latest consensus estimates suggest that MSCI China A-Shares are set to grow earnings by 18.1% in 2018; while offshore MSCI China stocks are expected to see growth of around 16.5%. While these estimates have a tendency to be overly optimistic with hindsight, they demonstrate that company fundamentals are solid at least for the near term. Valuations, on the other hand, suggest high levels of pessimism. Over the past eight months, P/E ratios for MSCI China and MSCI China-A have contracted by 24% and 28% respectively, a significantly more severe contraction than most other emerging markets. It is difficult to predict how much further sentiment could worsen; but one thing we can learn from history is that sentiment is very often a lot more volatile than economic reality. And we believe we are getting close to the point of inflection. The PE and PB ratios of MSCI China A-Shares are now close to all time trough levels at 10.7X and 1.65X respectively. Since 2005, we have seen 4 cases when MSCI China A-Shares P/B dropped below 1.7x, and the index has provided on average 39% total return over the following 12 months, with returns in positive territory on each of the 4 occasions.

Past performance is not a reliable indicator of future results.

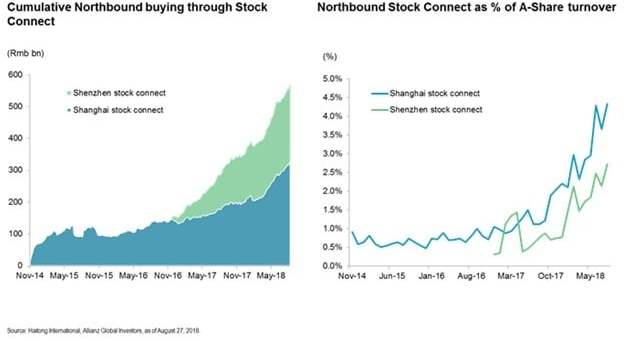

Amid the ongoing uncertainties, mainland China and foreign investors have adopted opposite responses to the market weakness. Domestic trading volume in China A-Shares has shrunk significantly to a multi-year low level, signaling extremely bearish sentiment by domestic retail investors. Weakness in China A-Shares has also had a spillover effect into the Hong Kong stock exchange – southbound flows (mainland investors purchasing HK listed stocks through the stock connect program) have turned to net selling since April 2018. On the other hand, domestic institutional investors are turning incrementally positive on China A-Shares. According to a JPMorgan survey in August, 73% of respondents expect a reverse of the downward spiral within the next 12 months. Foreign investors have sought to “buy the dip” in China A-Shares stocks. Year to date, Northbound investors (overseas investors buying into A shares through stock connect) have bought ~USD 33 bn of China A-Shares on a cumulative basis. The trend seems to continue, especially with index providers showing continuous support to accelerate the inclusion of China A-Shares. For example, on 26th September 2018, MSCI launched a new consultation to raise the inclusion factor of A-Shares large caps from current 5% to 20%. Another encouraging phenomenon is that China A-Share corporates are posting record buy-backs - more than RMB 55 bn (~USD 8 bn) year to date. While this is still very small in scale to compared to market turnover, it signals that companies are increasingly seeing value in their share prices and are increasingly committed to enhance shareholder returns.