February 2020

The outbreak of the Coronavirus (2019-nCoV) marks the first “black swan” event in 2020. At the time of writing there are more than 70,000 cases of diagnosed and suspected patients in China, and more than 2,000 have died (19 Feb 2020). The economic consequences have also been significant. At one stage the Chinese equity markets had corrected by 12% compared to the pre-breakout peak.

While the situation remains fluid, this analysis tries to gauge the potential impact of the virus outbreak on Chinese equity markets. In particular we compare the experience now with SARS in 2003, the most relevant comparison. We also highlight specific opportunities and challenges that are different this time.

17 years ago, SARS infected over 8,000 people and killed 774 around the world. The mortality rate for SARS was very high at 9.6%, much higher than the 1% or less level* of the current Coronavirus.

*Source: Wind, Allianz Global Investors, as of 19 February 2020. 0.7% refers to the mortality rate for non-Hubei area, which we believe is more representative given confirmed cases within Hubei are significantly under-reported due to lack of hospital facilities.

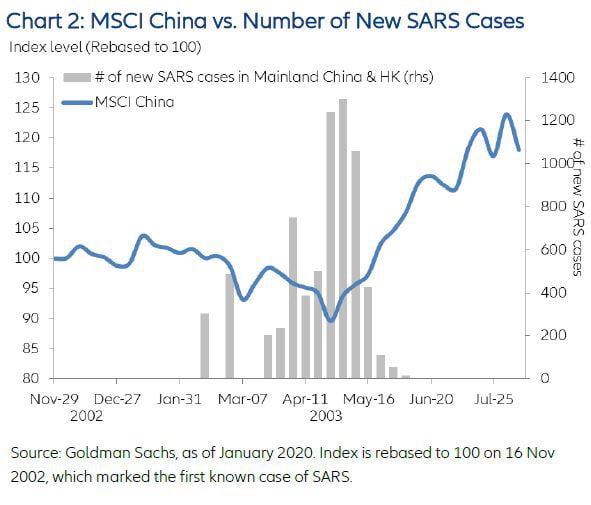

The SARS outbreak came to a stop in June 2003, when the warmer and more humid weather killed the virus. However, the Chinese equity markets bottomed earlier, in late April. This coincided with the peak number of daily new confirmed cases. It took the market around 4 weeks to recover to pre-SARS levels. To conclude, the impact of SARS on Chinese equities was sharp but short-lived.

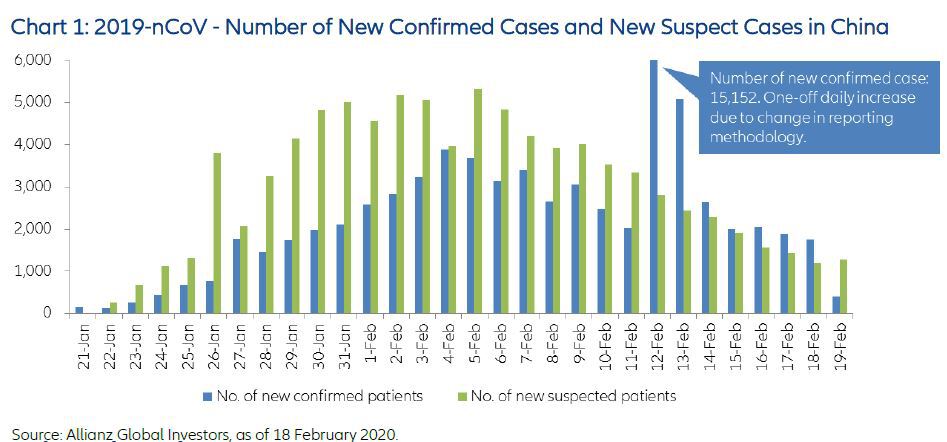

There are undoubted similarities with the 2019-nCoV situation. The peak of newly confirmed cases in China was on 4 February and there have been declines each day since then. Furthermore, the number of cases outside Hubei Province, where Wuhan is the capital city, has been declining since 3 February, indicating the containment measures have so far been successful.

The market reaction? After dropping 8% on 3 February when the Shanghai and Shenzhen stock exchanges re-opened post Chinese New Year, the CSI300 Index has since gained 10% (as of 18 Feb 2020), almost reaching pre-coronavirus levels.

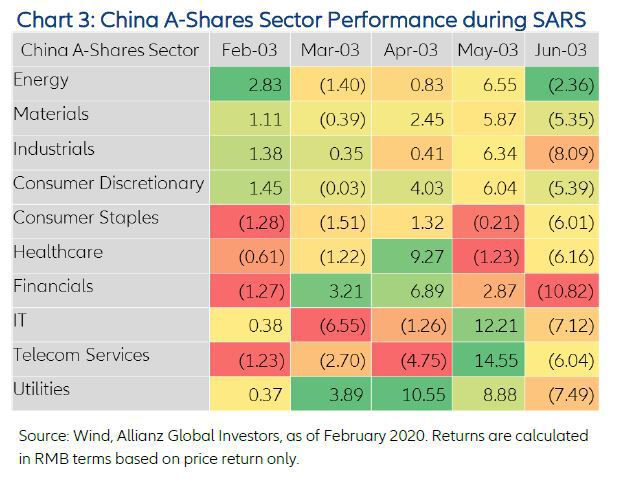

Another phenomenon we observed during the SARS outbreak was not only a high level of market volatility, but also significant intra-market volatility. It was not uncommon for the leading sector in one month to become the bottom performer over the next month. Of course the structure of A share markets has changed significantly over the last 17 years, but nonetheless retail investors are still dominant. So it would not be surprising to see history being repeated.

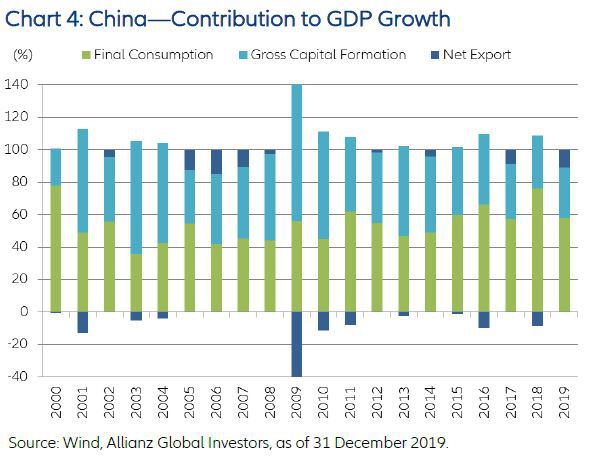

While the default mode is to look back at the dark days of SARS and seek parallels, in practice there are significant differences between now and then. From a global perspective, China has emerged from being a marginal player back in 2003 into a key engine of global growth. With China now representing ~19% of global GDP, slowing economic growth momentum will inevitably have a more significant global impact. This contrasts with the positive economic momentum in 2003, when China helped to lead the world out of recession. And within China, over the past 17 years domestic consumption has overtaken exports and fixed asset investment to become the main economic growth driver, representing around 60% of GDP.

The fundamental shift in China’s economic scale and structure means policy levers will likely have less impact compared to the SARS episode. Policy makers also so far seem committed to a prudent policy stance. We have seen modest monetary and fiscal easing, but nothing like previous stimulus packages, which led to excessive credit creation and a rapid increase in levels of debt.

Policies this time will likely be more targeted, including support for domestic consumption, stabilizing employment and providing incentives for small and medium enterprises though reductions of fees and taxes. Many companies will be required to do ‘national service’. Toll road companies, for example, have been instructed to waive fees. Banks will be forced to extend credit terms and so on. The impact should be to somewhat cushion the economic downside rather than leading to an economic acceleration as we saw post SARS.

A key difference between today and SARS is the change in government attitude. During SARS, there was a clear case of ’denial’. Government officials tried to cover up the real numbers of infected cases, resulting in a delayed response to combating the virus. This time around, the response could not be more different. It took 8 hours from the decision to quarantine Wuhan and the surrounding area comprising 56 million people, to put the region into lock down.

All around China, unprecedented measures have been implemented to contain the virus outbreak. At one stage it was estimated 750 million people had some form of restrictions imposed—from blocking roads, setting checkpoints, restricting people in high risk areas from leaving their homes and so on.

These government policies have been further amplified by the prominence of social media. Facts and rumors spread much faster than the virus itself over WeChat (the WhatsApp equivalent in China). The impact has been a ‘cover one’s back’ approach, both in China and around the world. More than 30 airlines have cut their services to China. None did during SARS. The result, therefore, is likely to be a much sharper economic downturn in China than with SARS— which helps to explain the recent change in emphasis from China’s leadership towards getting the country back to work.

For many smaller enterprises in China, the key now is economic survival. Companies with weak balance sheets and low working capital reserves are quickly running out of cash. They are facing multiple challenges—a collapse in demand, supply bottlenecks, labor shortages and wage pressures. According to a recent survey conducted by Tsinghua and Peking Universities based on 995 small and medium enterprises, less than 10% have cash reserves that will last more than 6 months.

In contrast, companies with robust balance sheets, capital discipline and strong supply chain management capabilities are likely to gain share. The trend to industry consolidation will likely accelerate, benefitting industry leaders. Listed companies should overall be more resilient than the non-listed universe.

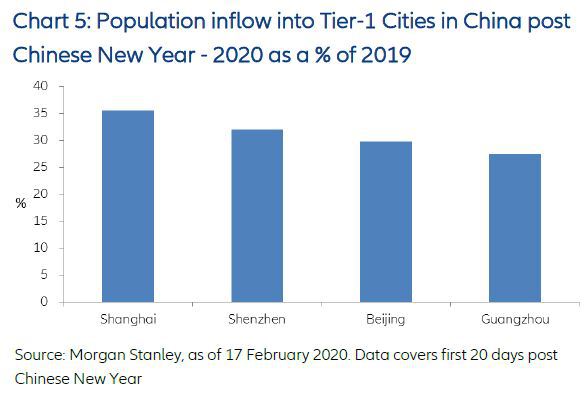

For the economy as a whole, it is important to monitor the progress of work resumption in China, which varies significantly across different regions and industries. So far only one third of the population has returned to work in tier-one cities. Other indicators such as Baidu maps traffic levels also remain sluggish. The coming days and weeks will be decisive in terms of the extent of the country’s downturn, and indeed the world’s, as Chinese companies form an integral part of the international supply chain.

We hear a lot of comments that you can’t trust the Coronavirus data from China, and that the number of cases is deliberately under-reported. Our view is different. The punishments in China for not reporting cases of 2019-nCoV are extreme. And having taken the decision to bring the economy to a halt, it would be hugely embarrassing for China’s leadership if the virus is less severe than expected. So if anything, government officials in China are now incentivised to over-react to cases of the virus.

There is also an important distinction between what is happening in Hubei province (Wuhan) - where the scale of the problem, with even basic medical services barely available has made it almost impossible to know the true numbers —and the rest of China, where the data is likely to be far more accurate. This is particularly important because outside Hubei, the data has shown a clear improvement since the peak on 3 Feb when there were 890 new diagnosed patients. The latest figure was 45 new patients on 19 Feb.

While the outbreak of SARS is probably the best reference for investors to gauge the financial and economic impact of 2019-nCoV, there are significant differences between now and then. We expect the economic downturn to be sharp but relatively short-lived in China, but the policy response will also be more limited. China A share markets are now trading close to their levels pre-Chinese New Year. This reflects growing market confidence that within China the virus has been contained. However, many smaller sized enterprises will struggle to survive the current crisis; therefore industry consolidators should gain market share and ultimately outperform peers. Intra-market volatility and sector rotation is likely to persist. Overall, we believe the economic value of the businesses we invest into should not be impacted, and therefore significant market or specific stock weakness is likely to be a long term buying opportunity.