January 2019

2018 has been a challenging year for investors in China equities. However, we believe the fundamental logic of investing in China for its long term growth potential remains intact.

This update includes an update on China’s structural growth drivers from the perspective of a Chinese millennial - Innovation, consumption upgrade and the rise of domestic brands. We also discuss how investors can look to access these secular growth drivers, many of which are well represented in China’s A-Share markets.

Yes, the China consumption story has been discussed for a long time. But we believe it is evolving. The consumption upgrade thesis is not just a function of higher income levels; it is also fundamentally tied to a change in consumer behavior, evolution of demographic structure, and the adoption of new technology. This is why we continue to see opportunities within the consumption upgrade trend, despite a moderation in China’s overall consumption growth.

Young, wealthy Chinese are turning their backs on traditional shopping in favor of spending their hard-earned cash on entertainment, travel, e-commerce and healthy living. Cultural experience, beautiful nature and tasty food have become popular ways to escape from the hassle of city lives. In 2017 alone, there were 5 billion tourist trips within China, tripling the level ten years ago. Overseas travel is also increasingly popular—as no doubt you will have noticed from the number of Mandarin speakers at tourist attractions and airports! The potential is still significant - only 9% of Chinese citizens have passports 1, which are essential for anyone to go across the border. Airline operators and travel agencies are the intuitive investment beneficiaries. A good example which we uncovered back in 2015 was China International Travel Services (CITS), the only nationwide duty-free store operator in China. This company owns airport duty free stores in major ‘tier 1’ cities in China including Beijing, Shanghai and Hong Kong. It has also opened the largest outlet within the domestic duty free zone in Hainan, the only province with tropical weather in China. Visitors to Hainan can now combine their beach holiday with a duty free shopping experience, doubling up the pleasure! Over the past three years, CITS has steadily lifted its earnings by 20% every year 2 thanks to the rising demand for leisure and travelling.

For illustrative purposes only.

When investors think of online shopping in China, they often think of Alibaba, the world’s leading e-commerce platform operator. The reality is that many bricks and mortar stores in China are also actively integrating online shopping as part of their long term strategy. A good example is the fresh food sector which is still at an early stage of development (Exhibit 2). As an example, Yonghui Department Store, a leading fresh goods superstore operator in China, is extending its in-store services to online – with a few clicks on the mobile app, consumers can now expect fresh lobsters and steaks to be delivered to their doorsteps within 30 mins from a close by store 3. And they can even choose to have the food cooked before delivery. Most of the times, delivery is free and you can’t even use cash to pay—everything is linked to e-payment.

The integration with online technology allows a traditional store to kill two birds with one stone: customers build strong loyalty around the convenient and customized services; while single store operating efficiencies can improve significantly with rising online orders. It is natural for such new retailers to gain market share from traditional operators, and become the winners of the future.

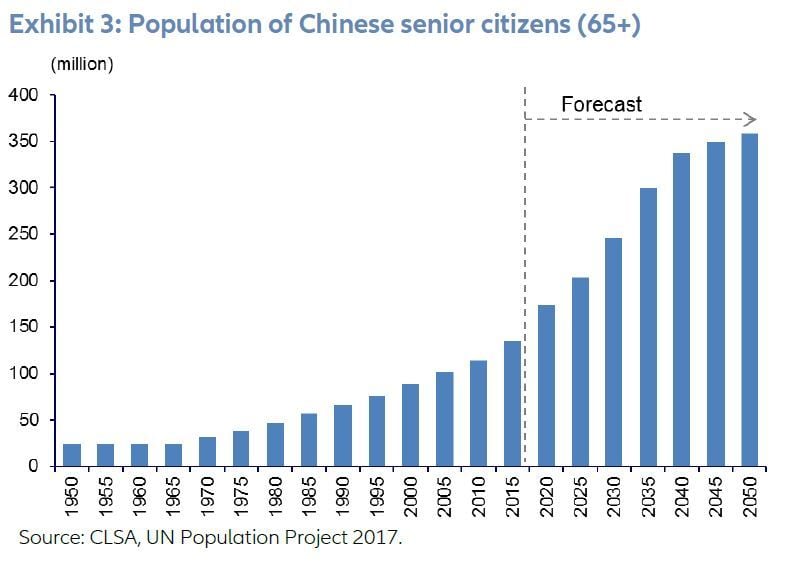

China spends far less on healthcare than more developed countries. In 2015, China only spent 5.3% of GDP on healthcare, compared to 9.9% in the European Union and 16.8% in the US. The average annual per person healthcare expenditure is only USD 426 in China, which is less than 5% of the US level of USD 9536 4. A rapidly aging population is making the situation even more challenging. Most millennials, who typically are the single child in the family, will need to think about how to support their parents and grandparents. By 2050, China will have 487 million senior citizens, making up 35% of the total population and adding more burden to China’s healthcare system 5.

Such a significant and inevitable demand-supply gap is creating a sense of urgency for healthcare providers to innovate fast. Take the pharmaceutical sector as an example. Currently the best selling drugs in China are still traditional Chinese medicine and low-end chemical generic drugs. But that balance is starting to change. China’s Food and Drug Administration has accelerated drug approvals— over 35 major new drugs were launched in 2017, as compared to 5 nationally approved drug launches in 2016 6, mostly by multinational corporations. Local pharmaceutical companies are beginning to innovate as well. For example, the number of applications for local innovative drugs entering clinical trials in China has grown from 21 in 2011 to 88 in 2016, a compound annual growth rate of 33% 7. A strong product pipeline combined with accelerating demand for better medication means there is still attractive room for growth, especially for companies with strong research and development capabilities.

It has long been the case in China that foreign brands are seen as superior in quality and therefore more desirable, despite the much higher prices. And in many areas that is still the case. The long queues at tax refund counters in airports around the world show the ongoing demand for foreign goods. However, there are definitely signs this is changing. The pressure from Chinese consumers and corporates for higher quality and better service is forcing an upgrade in domestic manufacturing. Indeed, in some particular areas, domestic brands now trump foreign names in terms of product quality, suitability and competitive pricing. In 2008, 90% of smartphone sales in China were from three foreign brands: Nokia, Motorola, and Sony. Now 8 out of top 10 smartphone brands are Chinese, with Huawei, Oppo, Xiaomi and Vivo leading the pack (Exhibit 4).

A similar trend of “foreign substitution” is happening within the manufacturing space as well. In select industries, Chinese companies are already competitive in terms of quality when compared to foreign players. For these domestic leaders, a superior service level and strong sales network, rather than deep price discounts, have typically become the main competitive advantages.

As a specific example, within the heavy machinery industry top Chinese players are already leading the market. Sany Heavy, the largest excavator brand in China, now tops the market with close to 1/4 of market share, larger than US brand Caterpillar 8. The largest laser equipment provider in China is also taking market share from Taiwanese peers and now offers similar quality equipment compared to German brands. Their laser equipment is now used to carve the logo on the back of Apple iPhones. And the technology is being extended into other areas such as electrical vehicle batteries and industrial automation. Another good example of foreign substitution is the car industry. As the quality of Chinese cars has improved, so has their market share. Chinese brands had 21% of the passenger car market 15 years ago, compared to 42% in 2017, especially at the expense of Korean and Japanese players. This ratio is even higher when it comes to new energy vehicles (NEV) - in 2017, for every 10 NEVs sold in China, 9 were local brands (Exhibit 5). Of course at the luxury end of the market, it still sends a strong signal to be able to afford a BMW or a Tesla, but this is a clear signal about how the gap is closing.

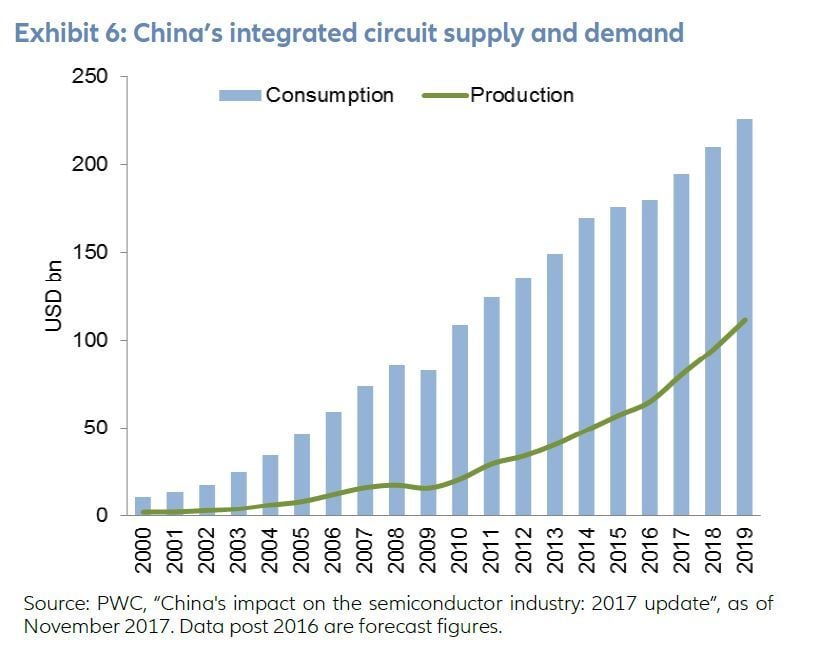

The trend towards substitution of foreign players with technology at home has paved the way for Chinese manufacturers to enter international markets. There is certainly a long way to go for most Chinese companies to achieve this target; however, there are already early signs it is happening in some areas. Chinese electric vehicle battery maker Contemporary Amperex Technology (CATL), for example, has recently announced it will build its first production site in Germany, agreeing a major contract with BMW to supply lithium-ion batteries 9. There are of course many other industries where Chinese homegrown technologies are still far from the level needed to meet local requirements. Around 2/3 of semiconductors consumed in China have to be imported—In 2017, China imported USD 260 billion worth of semiconductors, more than its $162 billion imports of crude oil 10. Almost all commercial aircraft in China are made by Boeing and Airbus. The most recent home-made commercial aircraft C919, which completed its maiden flight in May 2017, is not expected to enter commercial operation until at least 202111. Even within the industrial robotic space, which is a key element of smart manufacturing, Chinese manufacturers represent only 1/3 of the domestic market and are still highly dependent on foreign suppliers for critical core components 12. There is still a steep learning curve for most Chinese companies in these fields before they become truly competitive.

China’s ambition to strategically build up its ‘smart manufacturing’ capability is reflected in President Xi’s “Made in China 2025” program. This is designed to increase China’s self-sufficiency—a philosophy which can only be enhanced by the disputes in 2018 with the US. “Made in China 2025” prioritizes 10 industries including robotics, chipsets, biotech and renewable energy, which aim to become mainly domestic based by 2025. Concrete benchmarks have been set for the progress towards self-sufficiency - 40% of mobile phone chips within the Chinese market should be domestically produced by 2025, as well as 70% of industrial robots and 80% of renewable energy equipment (Exhibit 7).

While there are always questions about whether such a centralized program can lead to an optimal allocation of resources, what this does provide is a clear indication of policy direction in coming years. In terms of potential investment opportunities, there are clearly companies that can benefit from these forceful policy tailwinds to gain technological competiveness, especially in areas such as industrial automation and electric vehicles which are already benefitting from government subsidies to build up their production base.

The race for technology supremacy is clearly now at the heart of the trade conflict between China and the US. And it is very likely there will be a tightening of intellectual property transfer around the world. Therefore increasingly China will be dependent on more domestic-based factors for innovation, including a sufficient pool of research and development talents, strong funding support from capital markets, as well as favorable policies from the government.

No doubt this will present certain challenges, but China’s long term planning and sheer scale do provide some advantages. In 2017, China had 8 million college graduates, more than double of the number in the US 13. China is also home to the highest number of STEM graduates, i.e. those specializing in Science, Technology, Engineering and Mathematics 14. And in terms of funding support, China is now the world’s second largest spender in R&D with USD 279 billion spent in 2017, just after the US15. In regard to some of the most innovative technologies and growth industries—financial technology, virtual reality, artificial intelligence, robotics—China is comparable to the United States today in terms of venture capital investment.

Investors have increasingly come to realize that China’s growth story is beyond just the internet giants. As we have discussed in detail above, in order to more comprehensively capture China’s secular growth, investors have the option to dive deep into areas including consumer goods, services, healthcare, smart manufacturing and technology.

As illustrated by Exhibit 9, Hong Kong hosts a disproportionate amount of China’s more mature, ‘old economy’ stocks in sectors such as real estate, banking, telecom and utilities; while China’s tech giants are better represented on the New York stock exchange. China A-shares, those companies listed on the Shanghai and Shenzhen stock exchanges, represent over 70% of the consumer, healthcare and industrial sector opportunities, the latter including many of the ‘smart manufacturing’ companies.

We need to point out that 89% of revenue exposure of non financial China A-shares are domestic based. Using MSCI China A-shares Index as a proxy, only 2.5% of the revenue for non financial stocks are sourced directly from the United States. Going forward, we expect rising domestic demand driven by the consumption upgrade story, which in turn creates opportunities for domestic innovators that are continuously replacing foreign brands. Companies that can differentiate themselves through strong R&D capability, advanced business models and product innovation can therefore become the winners of the future. It is clear that for investors who want to tap into the China macro growth story, China A shares offer a significantly wider range of opportunities than ‘offshore China’.

1. Source: Goldman Sachs, as of December 31, 2017. 2. Source: Thomson Reuters, company reports, as of December 31, 2017. 3. Source: Fund Business Intelligence, “Yonghui Superstores – the vanguard of China’s grocery market”, as of November 2017. 4. Source: World Bank Database, as of December 31, 2015. 5. Source: CHINA-WHO, “Country Cooperation Strategy 2016–2020”, 2016. Retrieved on September 30 2018. 6. Source: McKinsey and Company, “What can we expect in China in 2018?”, as of December 2017. 7. Source: McKinsey and Company, “What’s next for pharma innovation in China”, as of September 2017. 8. Source: Allianz Global Investors, as of October 31, 2018. 9. Source: Reuters, “BMW agrees $4.7 bln contract with China's CATL for battery cells”, as of July 9, 2018. 10. Source: China Semiconductor Industry Association, General Administration of Customs, P.R. China, Allianz Global Investors, as of December 31, 2017. 11. Source: South China Morning Post, “Can ‘Made in China 2025’ help turn the nation’s domestic aerospace industry into a world leader?”, as of October 30, 2018 12. Source: Gongkong, as of December 31, 2017. 13. Source: China Ministry of Education, US Department of Education, as of December 31, 2017. 14. Source: Forbes, “The Countries With The Most STEM Graduates”, as of February2, 2017. 15. Source: CNBC, “China spent an estimated $279 billion on R&D last year”, as of February 26, 2018.