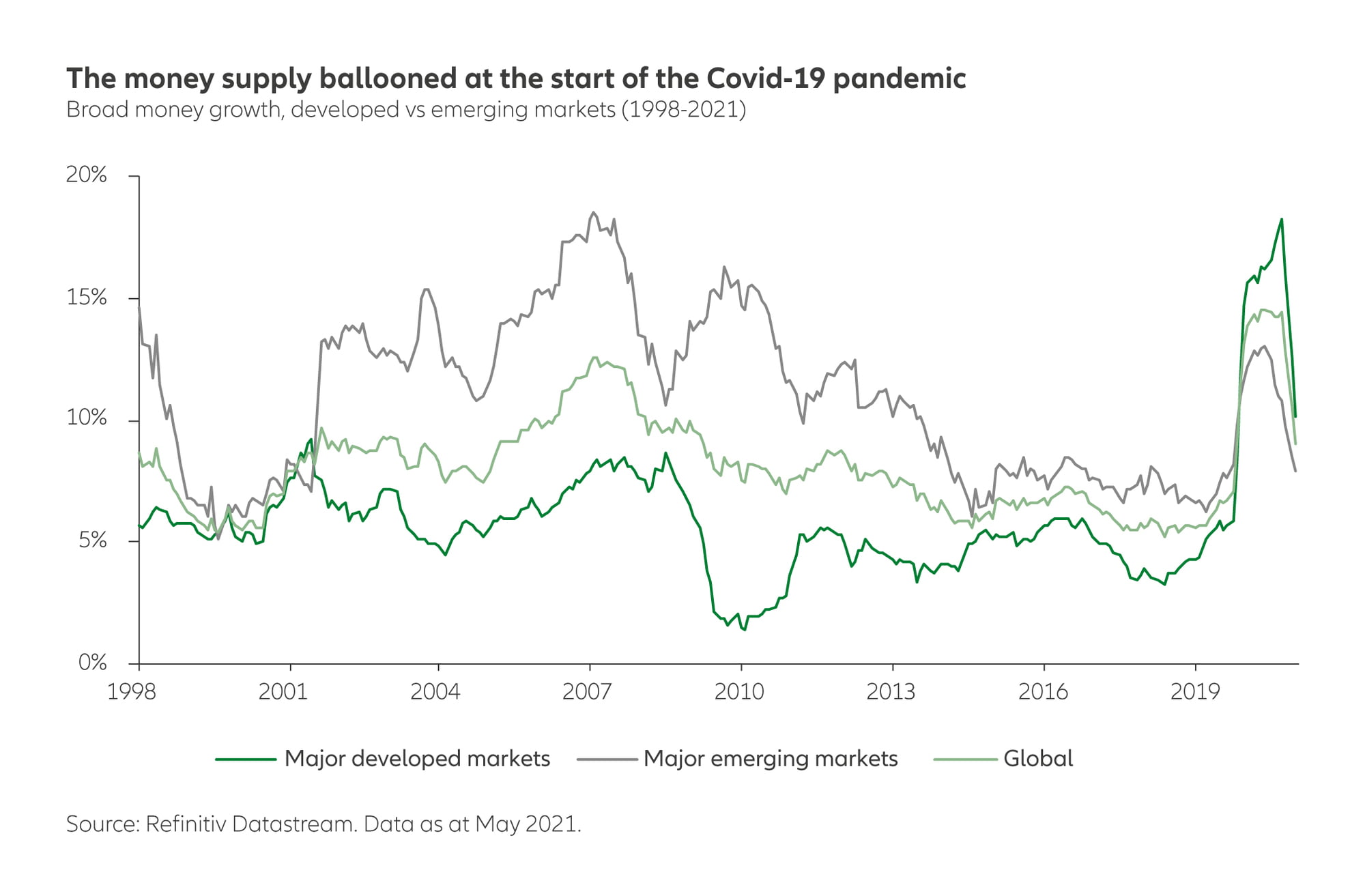

In response to recent economic crises, central banks have tried to stimulate growth. This can be seen in the massive growth in “narrow money” (such as coins, cash and highly liquid bank accounts) and “broad money” (which can consist of narrow money plus longer-term deposits). In fact, the money supply has grown at a rate that dwarfs any seen in peacetime. Strong money growth alone cannot cause higher inflation, but it is a precondition – in essence because there is more money chasing the same amount of goods and services.

Moreover, central banks have implied that they are willing to stay “behind the curve” for longer – meaning that they will deliberately not raise interest rates fast enough to head off inflation. Indeed, the US Federal Reserve has already announced that is accepting a temporary overshooting of the inflation rate through a policy called “average inflation targeting”. The European Central Bank is also comfortable with letting inflation overshoot its target.