Why Investors’ Understanding of China is Changing

Stefan Scheurer, Global Economics & Strategy

Then and Now: China’s Rebalancing Act

One of our economists, Stefan Scheurer, opened a wide-ranging debate on China by discussing how the Chinese economy has developed over time, and what it might look like in the future.

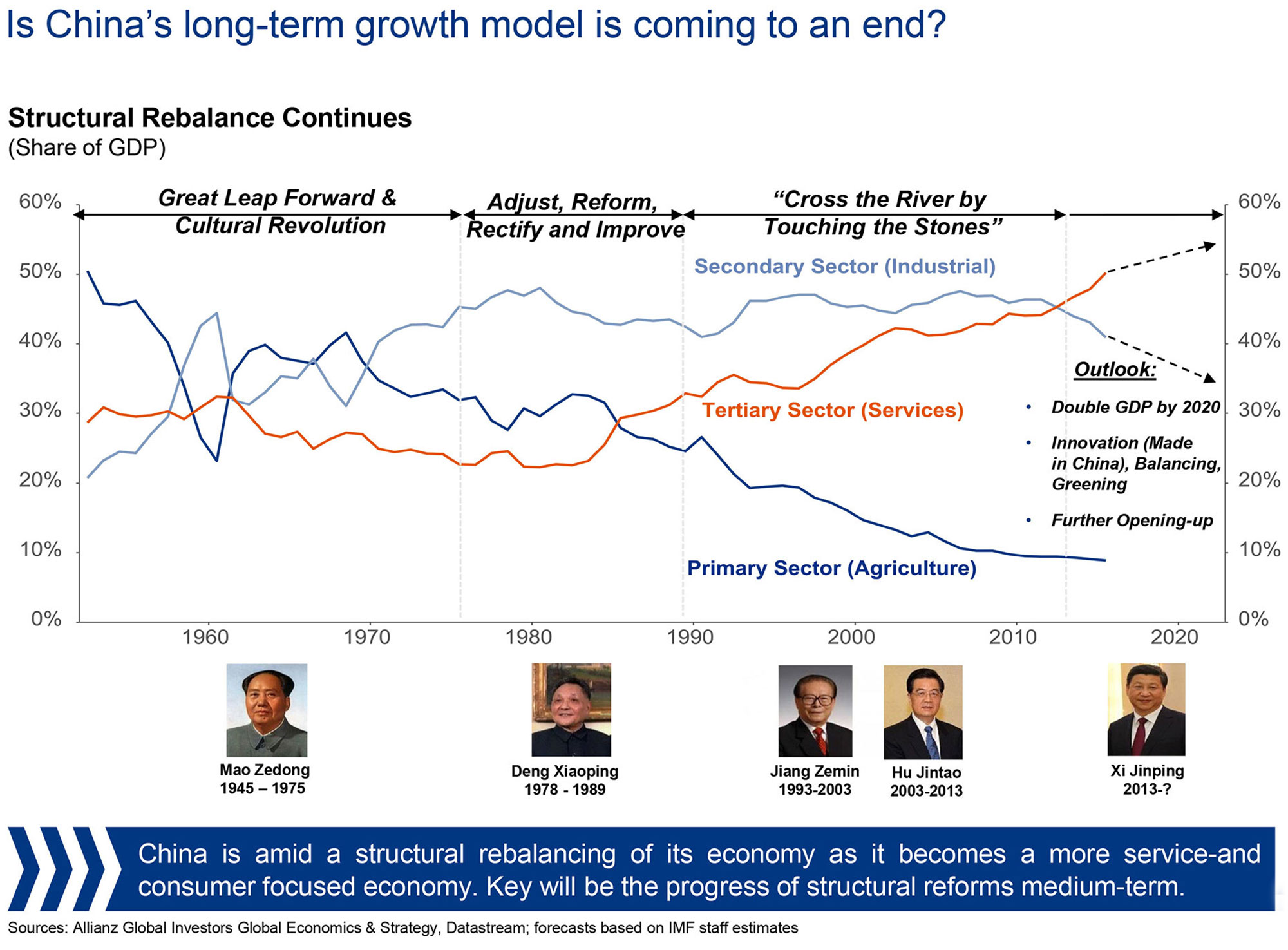

Stefan argued that China tends to think in decades. Historically, before industrialisation began in Europe in the early 1800s, China accounted for over a quarter of global GDP. However, China had been through a period of declining economic relevance, before reawakening in the 1980s. This was achieved by moving from an economy dominated by the agricultural sector, to an export-driven model, focussing on low-cost manufacturing.

China had remarkable success over the last decades using this growth model. China’s economy in 2010 was 17 times larger than in 1980, and 700 million people have been lifted out of poverty as a result. However, Stefan argued that China is now at an inflection point, and in order to continue growing it needs to transform itself into an economy focused on domestic consumption.

Figure 1: Structural Rebalance Continues

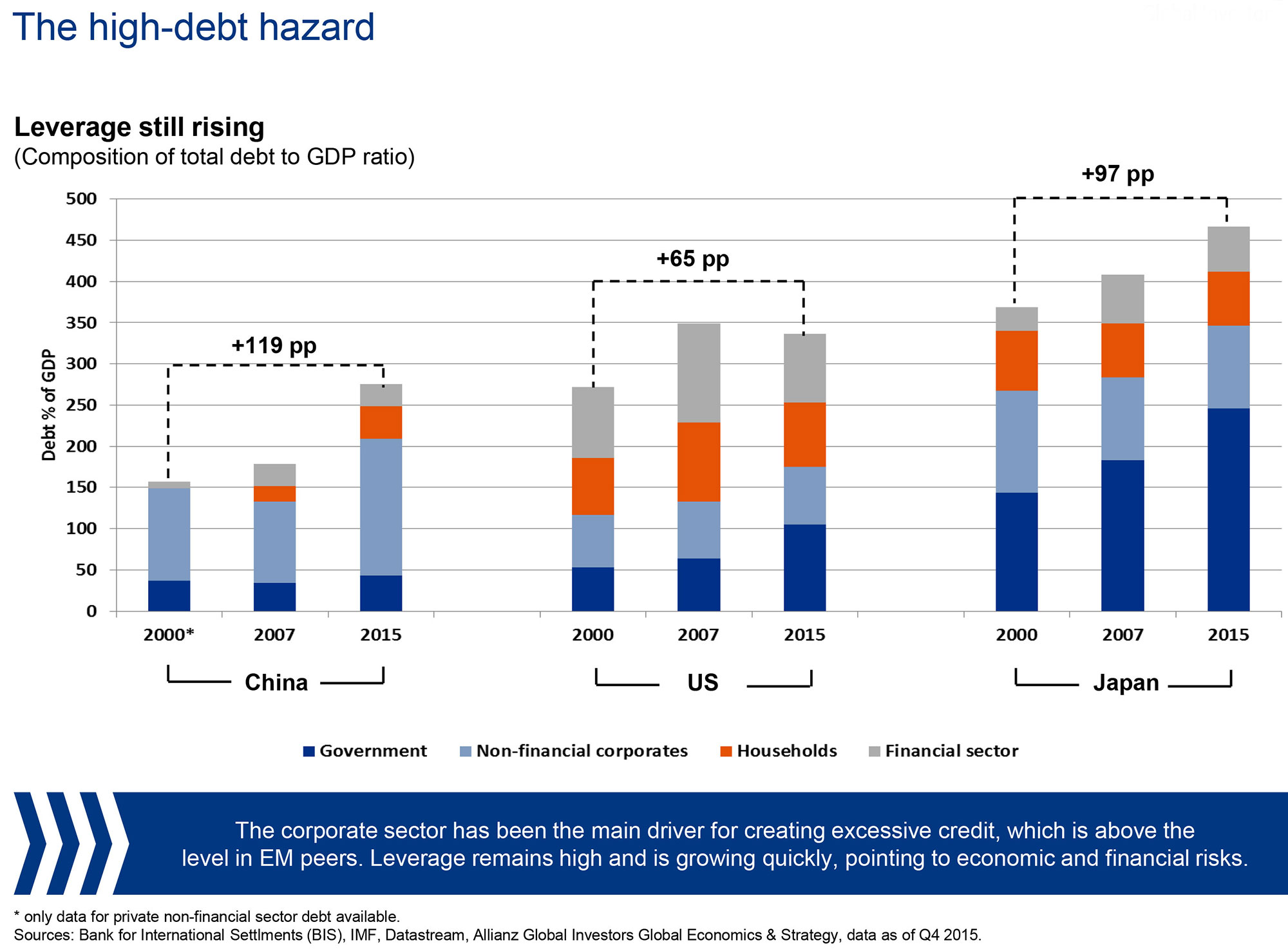

Figure 2: Debt-to-GDP 2000-2015

Stefan showed that while the growth of the Chinese economy has slowed over the last 10 years, its use of debt to sustain this has grown. Since the Financial Crisis, the US and other developed nations have deleveraged, but China has continued to create more debt. Debt-to-GDP in China is 119 percentage points higher than in 2000, mainly driven by the corporate sector.

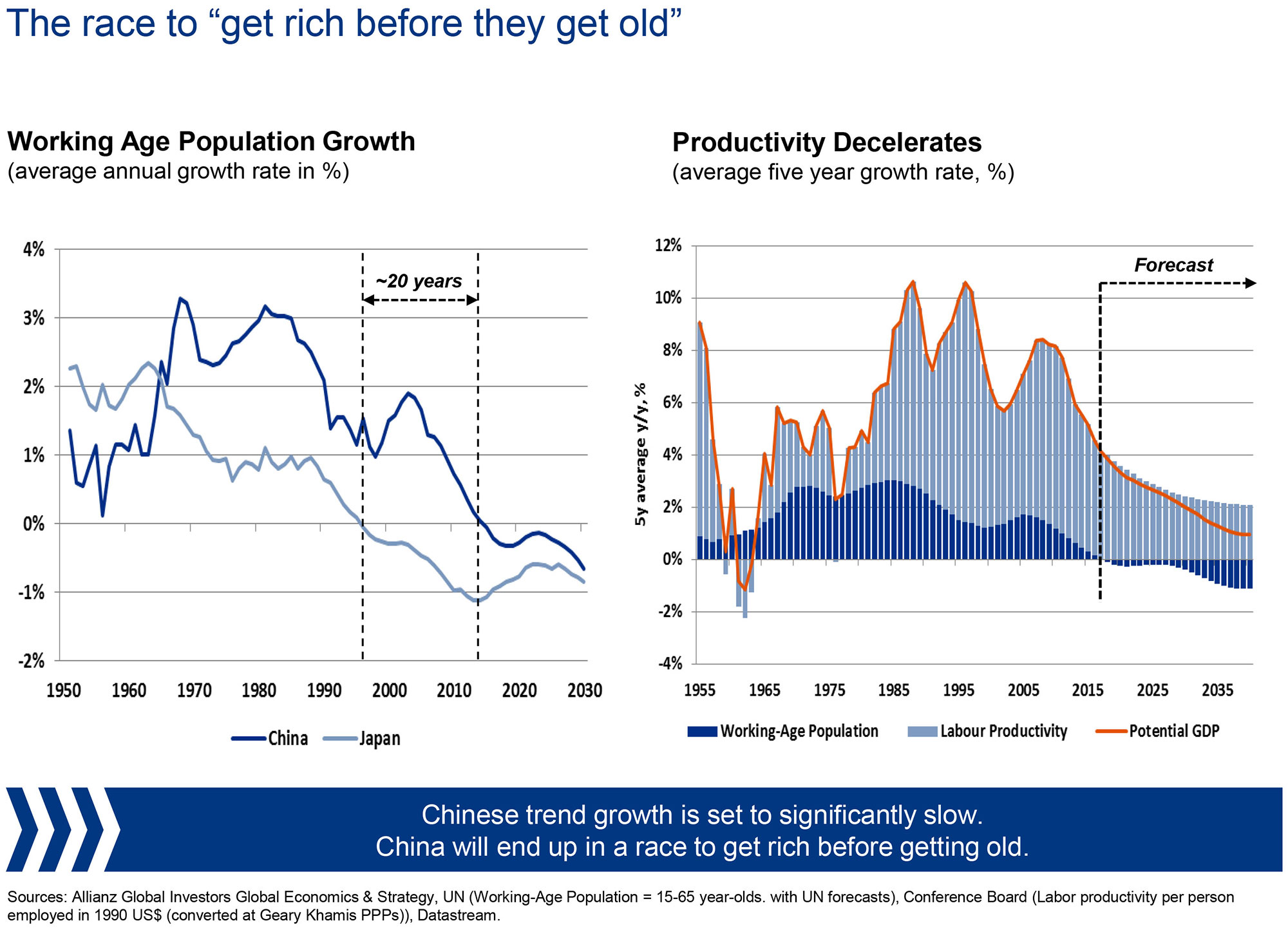

Figure 3: Falling population growth points to slowing GDP growth

Stefan believes that the reason China is using debt to fuel its economy is to ‘get rich before they get old’. China faces an aging population in much the same way that Japan did 20 years ago, which has the potential to drag down productivity.

Stefan expects GDP growth to continue to slow, and estimated it will reach a new trend rate of 3-5% p.a. in the next 10 years.

William Russell, Global Head of Equity Product Specialists

China as an asset class

The rapid growth of the Chinese economy could change how we approach investing in the market, claims William Russell, our Global Head of Equity Product Specialists. He believes that we need to start considering China as an asset class in its own right.

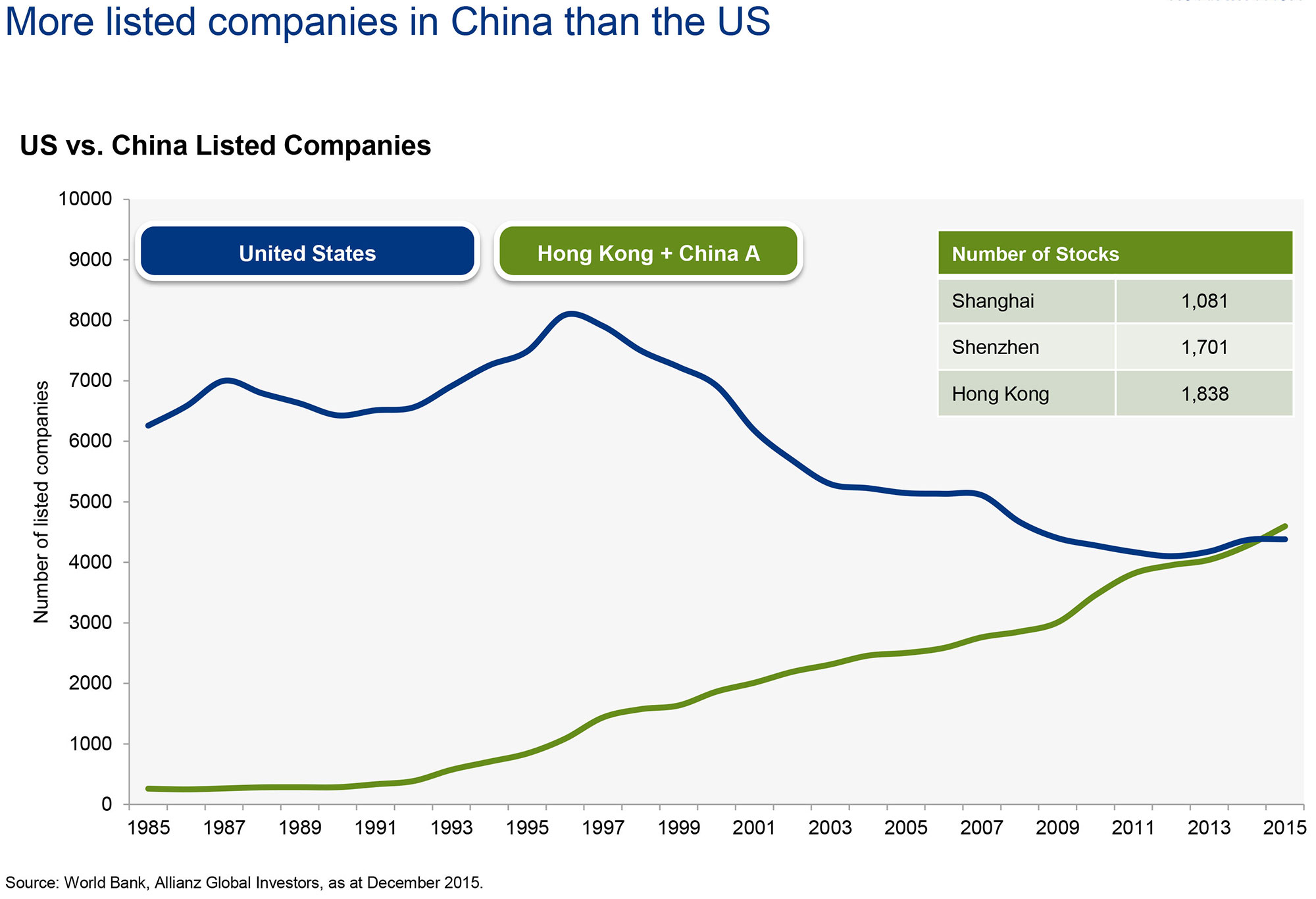

Chinese equity markets have continued to grow, and China now has more listed companies than the US. At the same time China has grown to be the second largest equity market as measured by market capitalisation. The story is the same in the bond market – China is the third largest issuer of bonds globally.

Despite representing 18% of global equity markets in market cap, many investors significantly underweight China in their global portfolios, driven by the fact that China only represents 3% of the MSCI AC World Index.

William discussed the reasons why China was a much smaller part of the index than its market cap: China A-Shares (shares issued in mainland China) are excluded from the index, with only H-shares and ADRs (American Depositary Receipts) included.

In China shares fall into two broad categories: China A-Shares and H-Shares. A-Shares are issued on the Shanghai or Shenzhen stock exchange, and trading is restricted to Chinese nationals, with international investors given small quotas. H-shares are issued in Hong Kong, with fewer restrictions on overseas investors. Clients currently access China by investing largely in China H-shares and ADRs.

Figure 4: Listed Companies and Market Cap

Figure 5: The Market Cap/Index Mismatch

Figure 6: Barriers to Entry are falling

But times are changing. William explained how financial reform and the opening up of the economy and currency to overseas investors was making investing in China A-shares easier.

In the future, William expects offshore and onshore equity markets to converge so that clients will invest in ‘Whole of China’. Clients want access to the best Chinese investment opportunities, regardless of where they are listed.

Figure 7: Performance Dispersion in Chinese Equities

Raymond Chan, CIO Equity Asia Pacific

Investing in Chinese Equities

Following the discussion on the development of China as an asset class, Raymond Chan, CIO Equity Asia Pacific, explained how Chinese equity markets are well suited to bottom-up stock picking.

Raymond showed that if we aggregate all the different types of Chinese equities there are 4,207 companies now listed in China, a 1,000+ increase since 2013.

The differences between types of Chinese equities present opportunities for experienced stock-pickers such as Allianz Global Investors.

Raymond explained that A-share markets are locally driven, whereas H-shares and ADRs are determined by foreign sentiment, usually driven by top-down macro opinions.

Investors should remain aware that A-share and H-share equities have very different risk/return characteristics, which can lead to share prices for the same company diverging across the different markets.

However, Raymond expected that equities will continue to converge in the medium term, making A-shares more attractive to international investors. As a result, ‘Whole of China’ strategies (which combine share classes) will become increasingly popular, and Allianz Global Investors is leading product development in this space.

Raymond also expected that investors will increasingly demand more sophisticated products, such as Multi-Asset and lower volatility strategies.

As financial barriers to entry drop, Chinese equity markets will go from strength to strength.

David Tan, CIO Fixed Income, Asia Pacific & Greg Saichin, CIO Global Emerging Mkt Debt

The future of the Renminbi

David Tan, CIO Fixed Income Asia Pacific, and Greg Saichin, CIO Global Emerging Markets Debt, discussed the situation in the Chinese fixed income market. Just as is the case with Chinese equities, fixed income is a large and rapidly growing market that has so far been largely ignored by international investors. China is currently the third largest bond market in the world, and set to grow to $15trn by 2020. David explained how defaults in the Chinese onshore bond market began in 2014.

This has led to increased credit differentiation in China, with spreads increasing since 2014, indicating improved capital allocation, but it is also something investors must be aware of when considering investing in this market.

Figure 8: Chinese Bond Market

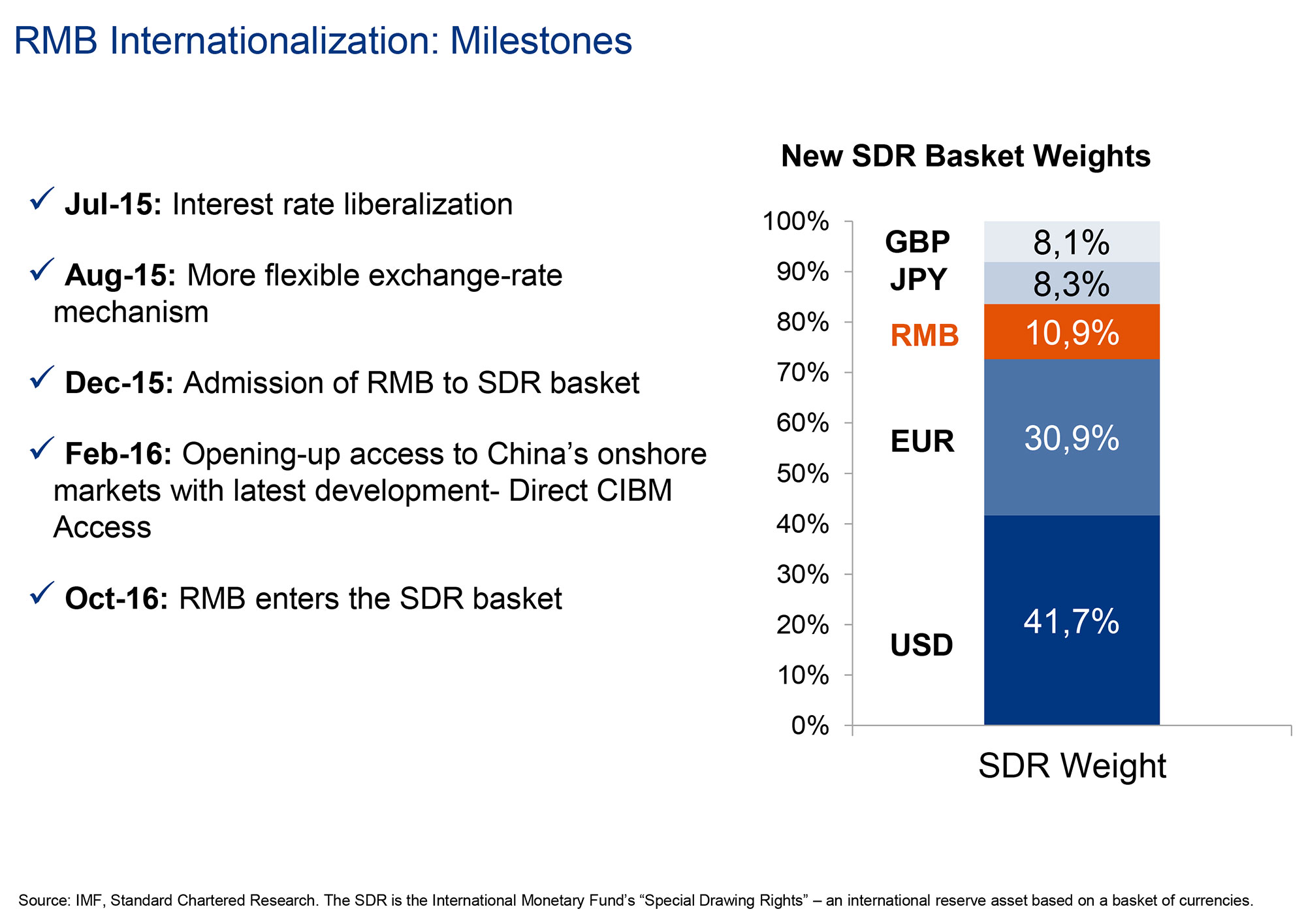

Figure 9: RMB Internationalisation Milestones

Both David and Greg argued that despite the opportunities in Chinese Fixed Income, more progress needs to be made in opening up the market to investors.

Some improvements have already been made. David discussed the process of RMB internationalisation, which has made buying Chinese assets easier for international investors.

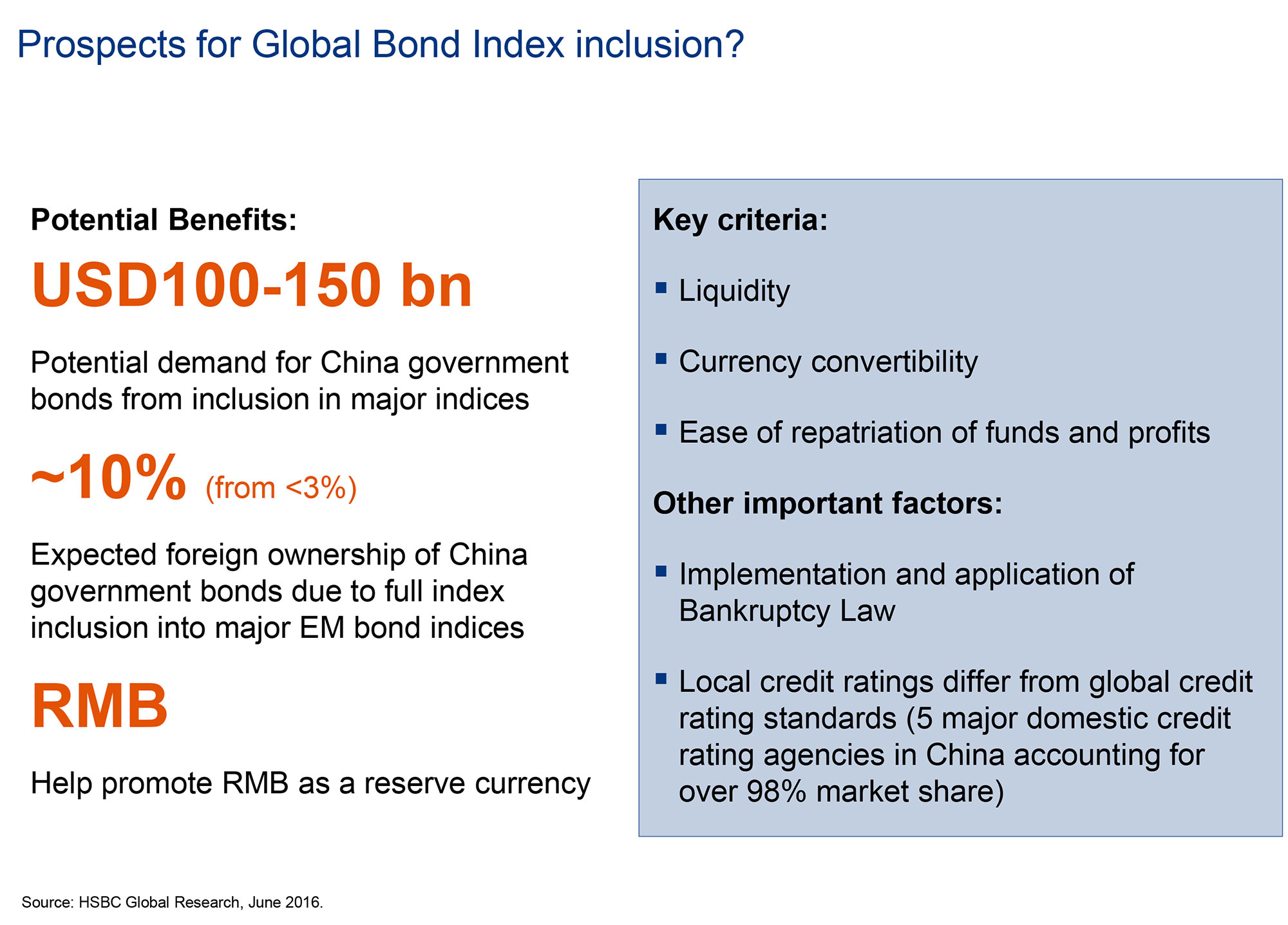

However, only 2% of the Chinese bond market is foreign owned currently. Greg argued that inclusion in global bond indexes is crucial for China, and he thought this could start occurring in the second half of 2018.

Inclusion will only happen if China continues on its reform path.

Figure 10: The Road to Global Bond Index inclusion

One of the clear topics of agreement amongst all the attendees was that China has changed the world with its growth over the last 30 years, and that it is now a significant global superpower. However, what is also clear is that the previous model for Chinese growth cannot continue, and this will impact how investors approach the country. In addition to changes in the economy, the changing approach China is taking to capital markets will have an even greater impact for investors.

As equity and fixed income markets open up and warrant greater inclusion in global indices, investors can no longer ignore them. An understanding of the dynamics at play in the domestic debt and equity markets will be crucial for investors, and it is becoming a real possibility that China may soon be an asset class in its own right.