Established Ways of Doing Business are Being Challenged

Gunnar Miller, Global Head of Research

Is disruption changing the game?

Gunnar Miller, our Global Head of Research, opened a discussion of disruptive technologies by discussing the impact disruption has on asset management. He described how our own industry has been impacted by the rise of indexing and increasing fee compression, along with tougher regulation and declining external resources, which have severely disrupted active investors over the last few years. But Gunnar argued that as well as looking at our own industry we also need to look beyond it. As investors, we are also affected by disruption in all industries, as business models and entire sectors are created and destroyed at an accelerating pace.

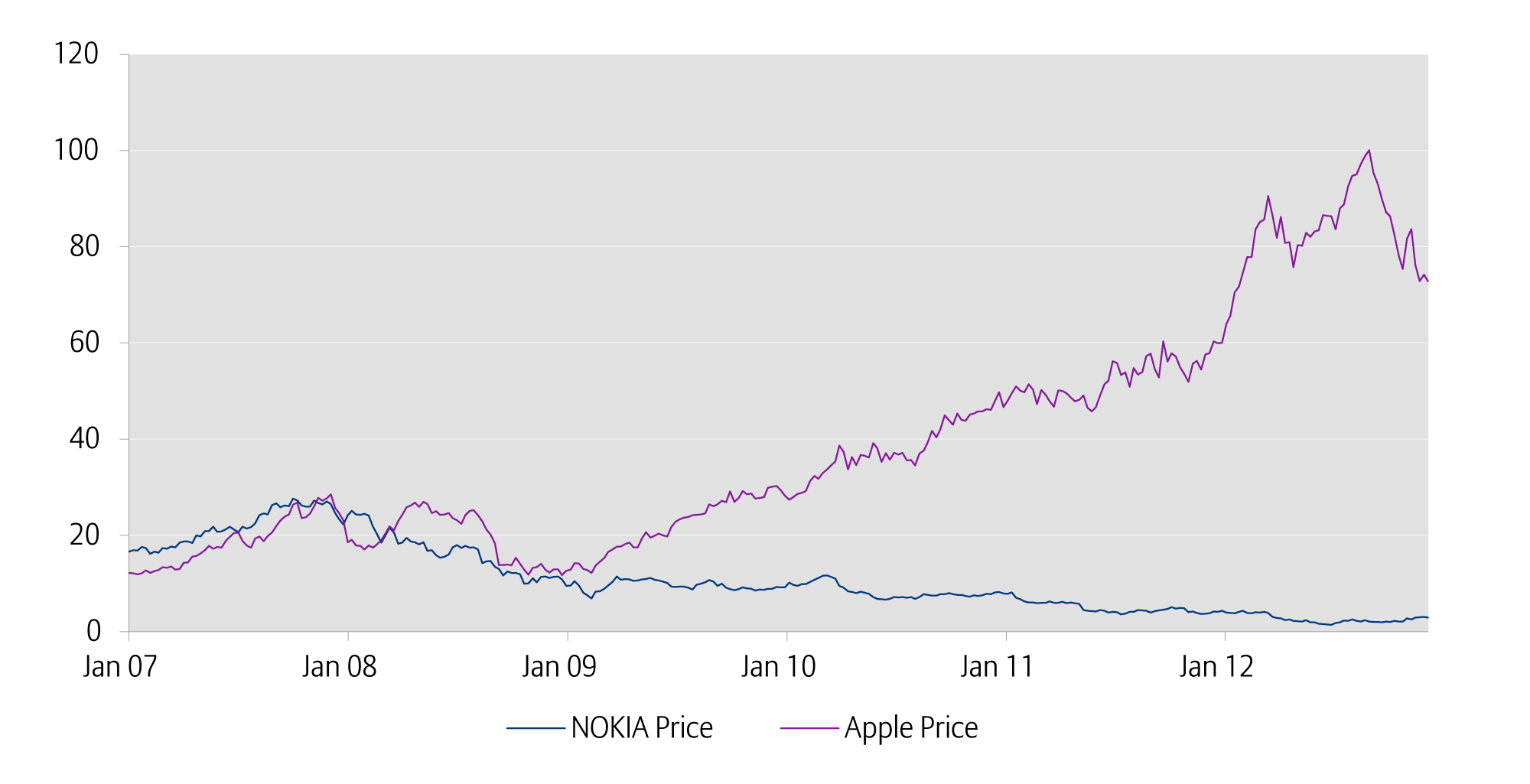

Gunnar used the example of Nokia as an illustration of why investors need to think carefully about disruption. He described how at its peak in 2007, Nokia controlled 41% of the global handset market, and would have been viewed as having below-average disruption risk prior to the iPhone. The share price at the time was €25. By 2012, the share price had fallen 94% to €1.50. With no process in place to flag to investors that the entire mobile telephone market had been disrupted, it became a classic value trap.

A value trap is a company that appears to be cheap and offering a ‘value’ investment opportunity. Typically this means the stock will be trading on low earnings multiples or price to book value. However, the stock can be a ‘trap’ if it’s actually in structural decline, and despite being cheap the share price never recovers.

Figure 1: Nokia vs. Apple share price 2007-2012

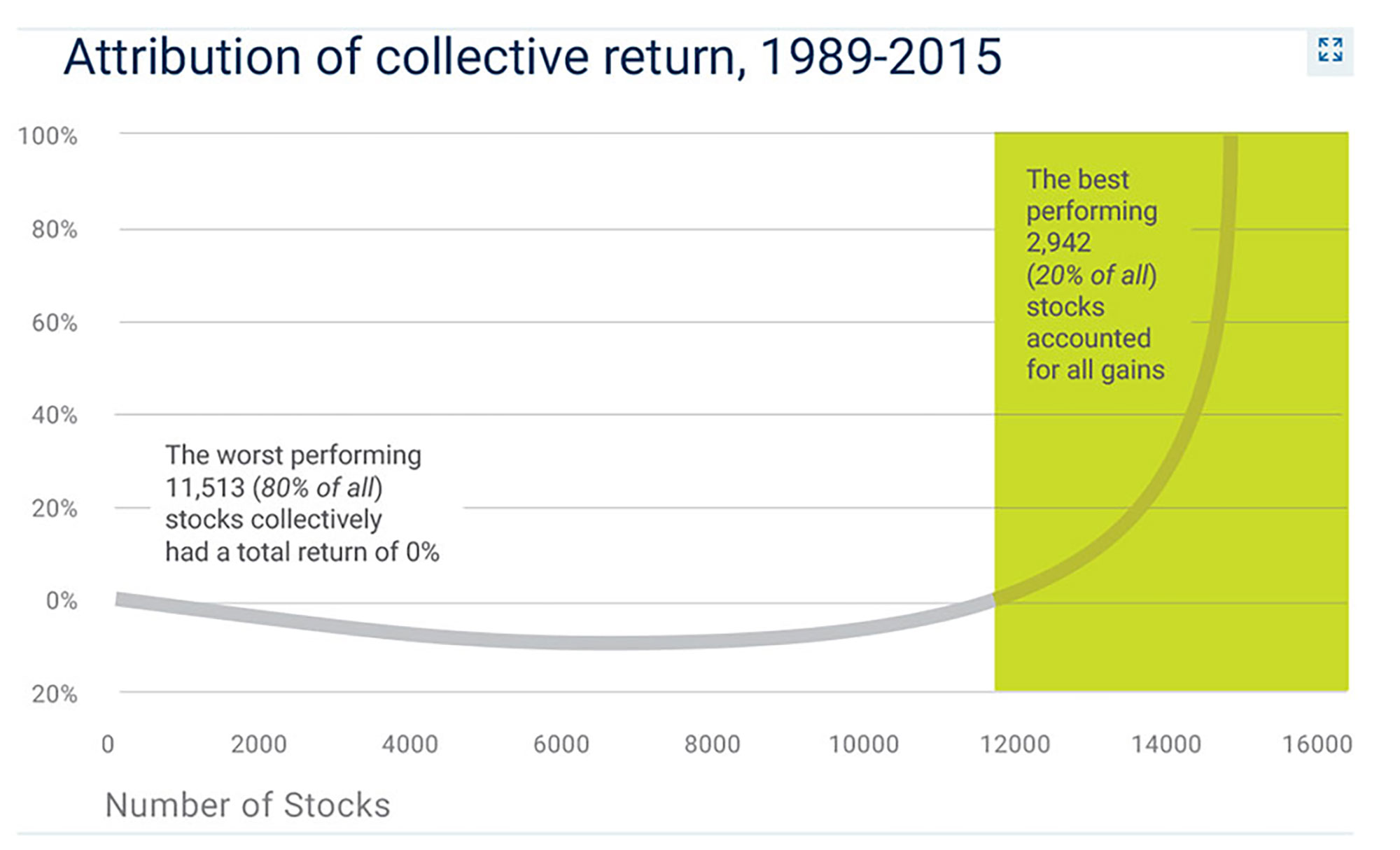

Figure 2: Attribution of US stock market returns

Gunnar described how the average company lifespan on the S&P 500 has been falling over time. In 1960 the average was 60 years, but by 1990 this was down to 20 years, and currently sits at 12 years.

Gunnar therefore argued that as business disruption accelerates, the importance of stock-picking grows. As Figure 2 shows, all the long-term returns of US equities come from just 20% of stocks. Over the long term, we feel that the best investment approach is to be active and avoid the underperformers, which passive investments cannot offer.

Figure 3: Attribution of US stock market returns

Gunnar concluded his talk by introducing our new ‘Disruption Risk Ratings’, which are part of the wider Intrinsic Ratings project at Allianz Global Investors. These new ratings provide every investment professional with a clear and current view of potential business model disruption over a 3-5 year horizon.

He explained how Disruption Risk Ratings are part of our broader Intrinsic Ratings project, where we are centralising our various non-financial valuation thoughts on companies together in one easy-to-find place in Chatter, our propriety platform for sharing investment ideas.

Sebastian Thomas, US Head of Technology Research and PM AI Strategies

AI and its Investment Implications

Sebastian Thomas, our US Head of Technology Research and Portfolio Manager of our AI strategies, continued the discussion on disruption by discussing Artificial Intelligence (AI), and what it might mean for investors like us. He explained how AI technologies made profound breakthroughs since 2012, such as Google’s Artificial Brain learning to identify cats in YouTube videos with 75% accuracy.

AI is the science and engineering of making intelligent machines, with a focus on intelligent computer programmes. Varying kinds and degrees of intelligence occur in people, many animals and some machines.

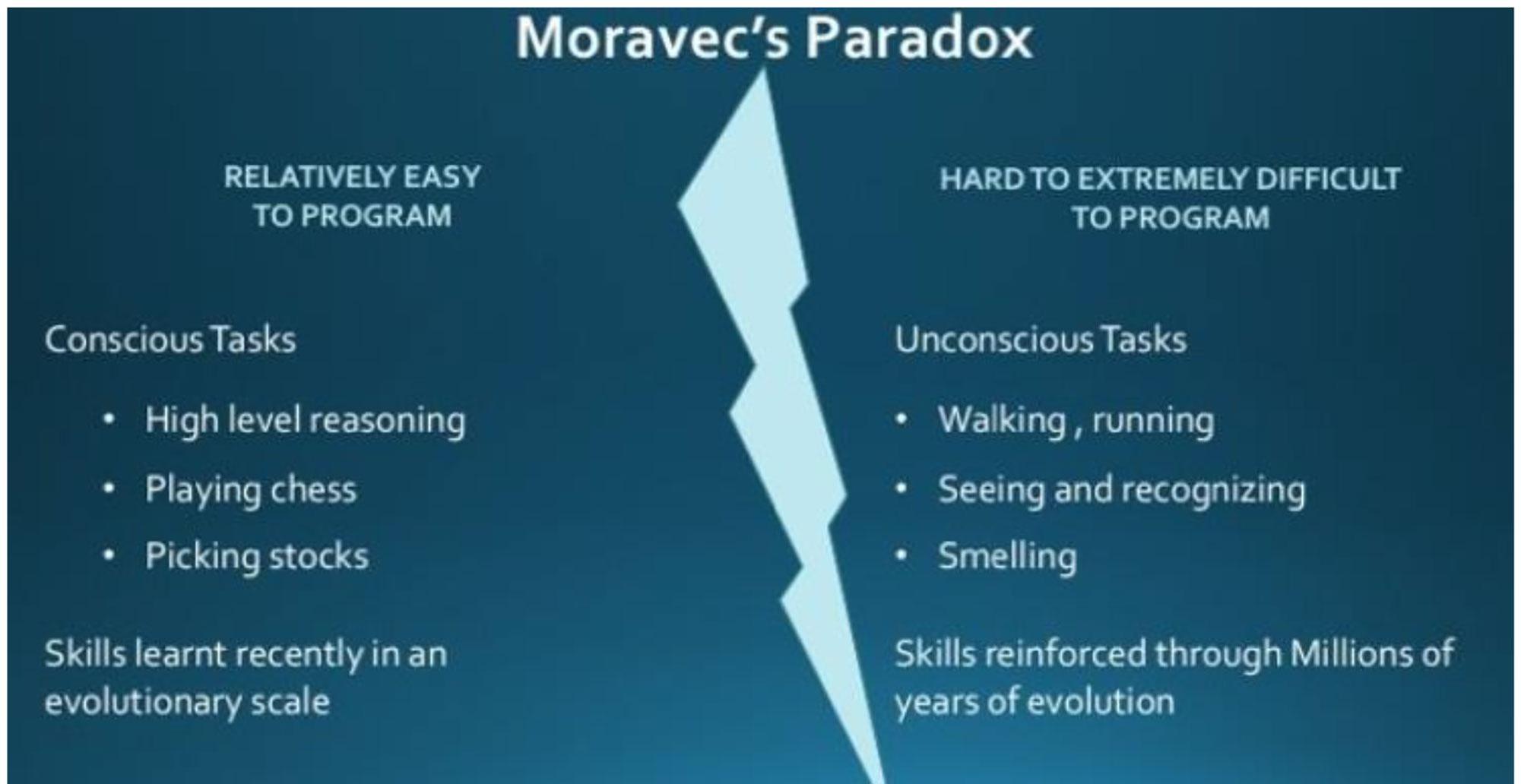

Sebastian described how this is part of an ongoing effort to solve “Moravec’s Paradox”: it is paradoxically very easy to make computers complete high-level reasoning tasks like playing chess, but nearly impossible to teach them to complete low-level tasks like walking or recognising people or objects.

Figure 4: Moravec's Paradox

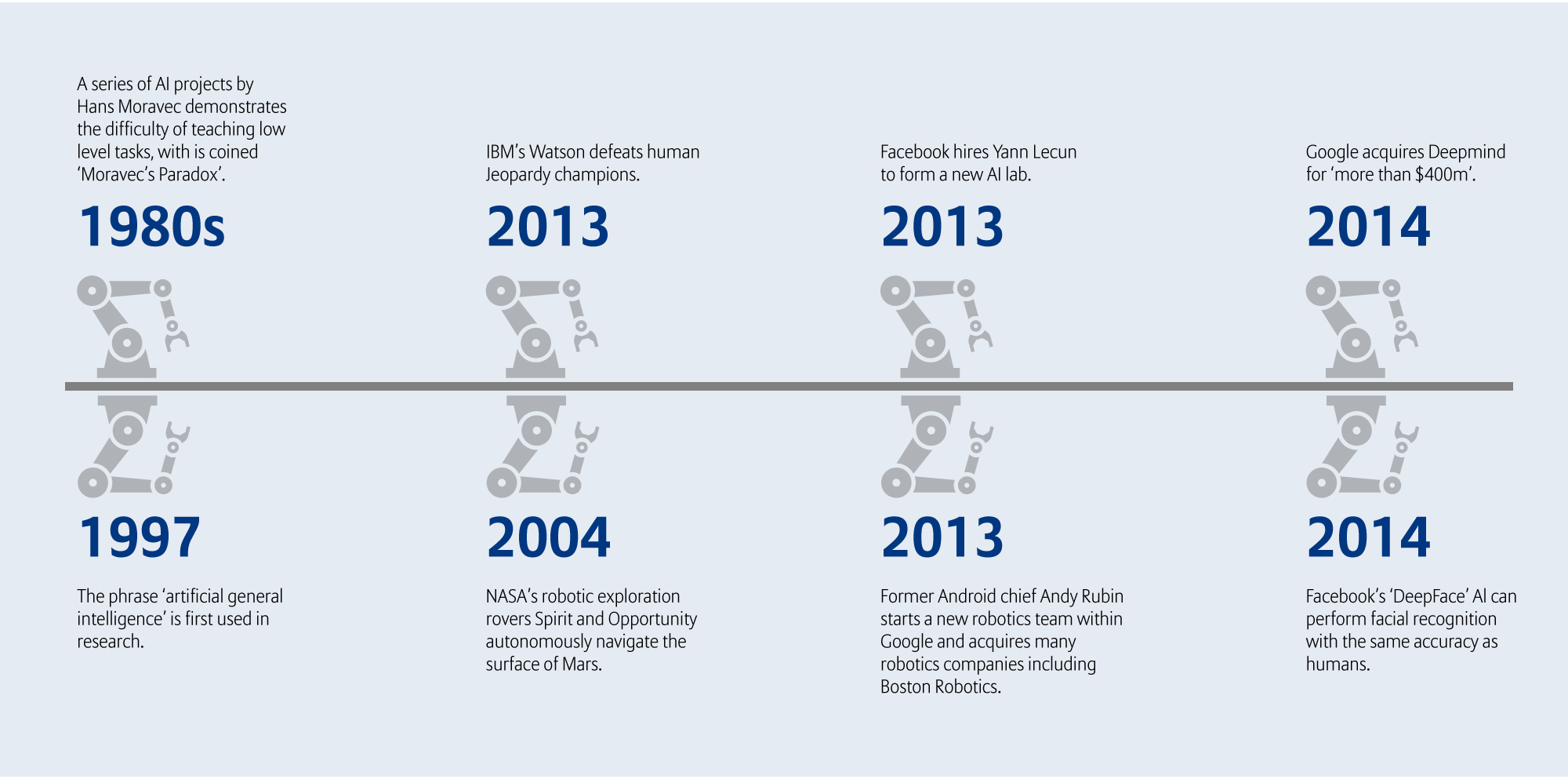

Figure 5: Timeline

Sebastian gave the example of the self-driving car to highlight the progress made in AI. Several leading manufacturers and technology companies are approaching a point where their technology is close to being ready, but the law and society at large is not prepared for the significant changes this could bring. Sebastian also made the point that self-driving cars would not only have an impact on manufacturers in terms of car design and ownership, but also on the insurance industry and the structure of labour markets in the transportation sector. Therefore a portfolio manager needs not only to consider investing in the company providing the self-driving car, but also the profound impact this might have across various areas of the economy.

Sebastian also explained how Allianz Global Investors were investing in these new advances in technology through the AI investment teams.

The rise of disruption has some clear implications for investors. It places extra emphasis on underlying investment processes, to ensure portfolios are not exposed to disruption risk.

Disruption is clearly here to stay, and we should expect faster business cycles, and companies being created and destroyed at an accelerating rate. At Allianz Global Investors we have looked at this closely, and are working to ensure that all our teams invest with disruption firmly in mind.

This is about avoiding value traps like Nokia, and also discovering the next big opportunity.