Lucy Macdonald

During the period, European and emerging market equities led market strength helped by further signs that global economic activity continued to improve. US equities were arguably held back somewhat by increasing political risks and uncertainties concerning the ability of President Trump’s administration to enact its policy agenda. Strong corporate results and better-than-expected US jobless claims and regional manufacturing data at the end of May helped calm the nerves.

In terms of sectors, Information Technology stocks delivered robust returns. Utilities and Consumer Staples also performed well. On the other hand, Energy lagged as oil prices failed to build on earlier gains.

During the period, the Federal Reserve raised US interest rates twice – in December and again in March – taking the federal funds rate to a range of 0.75% to 1.0%. In contrast, in December the European Central Bank (ECB) extended its bond-buying programme until at least the end of 2017, but reduced the size of its monthly bond purchases. Subsequently, rising inflation in the first quarter of 2017 led to speculation that the ECB would need to wind down these measures, with President Mario Draghi noting that the battle against deflation had now been won. The Bank of England and Bank of Japan left monetary policy unchanged.

Diminishing political risk following Emmanuel Macron’s victory in the French presidential elections and further signs of euro-zone recovery boosted the euro while US dollar weakened amid rising political turmoil.

Oil prices initially strengthened following the news that OPEC had agreed to cut production, but later weakened amid signs of rising US supply.

On a total return basis, over the period the portfolio’s NAV with debt at fair value rose 12.6%, compared to a 11.1% gain for the benchmark (50% FTSE All-Share Index and 50% FTSE World Ex UK Index until 21 March 2017, and 70% FTSE World Ex UK Index and 30% FTSE All-Share Index from 22 March 2017). Overall stock selection contributed positively, particularly in Financials, Technology and Consumer Goods, which more than offset a negative contribution from Consumer Services, Health Care and Telecommunications. Industry weights,

which are a result of bottom-up stock picking, also contributed.

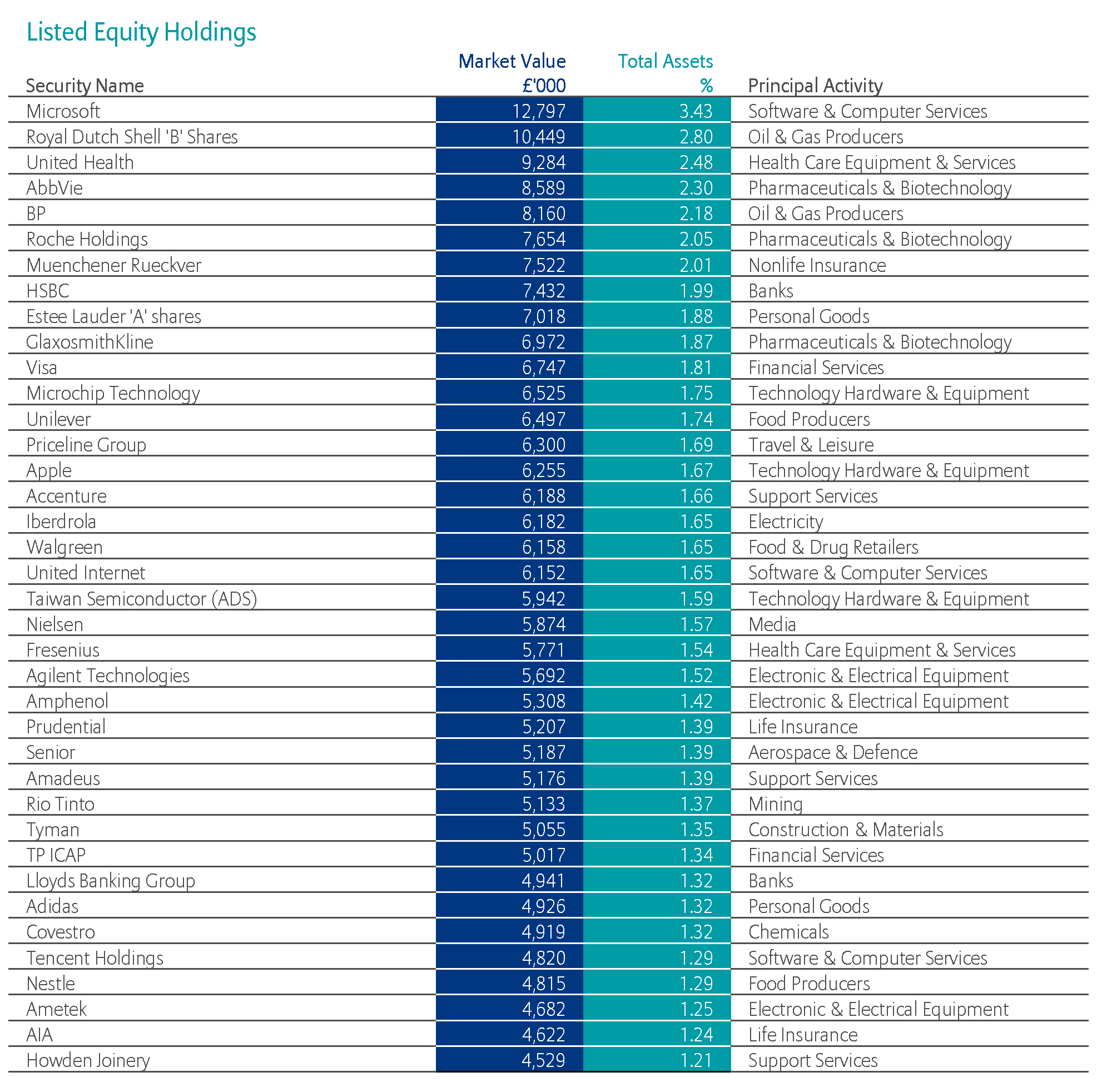

The top contributor to performance was United Internet, which announced the merger of their consumer telecom operations with Drillisch to gain strength in the telecom sector in Germany. This deal represents significant synergies and a solution for the issue of credible 4G wholesale access for United Internet, one of the major market concerns for the company.

Tyman was another strong contributor. FY16 results were strong, with margins in both the US and Europe ahead of expectations. This margin momentum looks set to continue as the US footprint project delivers more savings and synergies come through early. Management continues to benefit from self-help initiatives and plans to manage higher cost inflation through pricing, effective purchasing and cost reductions. The company has made significant progress structurally improving the business and we expect continued progress over the next few years.

Firstgroup, the US and UK ground transportation company, also outperformed. Full year results for the year to 31 March 2017 were better than expected, primarily due to better performances in North America. The share price has risen strongly in recent months: up 22% since it announced the South Western rail franchise win on 25 March 2017 and supported by a stronger dollar.

Nielsen was the top detractor. First quarter results came slightly below expectations as the company continued to experience weakness in the Buy segment, attributed to continued spending pressure from retail customers in the US. We view this as a short-term issue and the rest of the business remains strong; and we maintain our belief that Nielsen is one of the better positioned companies within the media sector, particularly given its leading position in the evolving and steadily growing Watch segment.

We reduced our exposure to the Energy sector in the first quarter this year and the underweight in the sector was positive to performance during the period. EOG Resources detracted, reflecting the overall fall in oil prices. EOG has grown mostly through internally generated projects over the last five years, only recently announcing their acquisition of Yates Petroleum. Given the potential of its portfolio, we still see EOG as a compelling investment.

Walgreens Boots also underperformed. While the Rite Aid acquisition, which would represent good synergy opportunities for the company, is still pending on the government’s authorisation, speculations that Amazon is looking to enter the pharmacy market could represent a market disruption in the retail pharmacy business, directly affecting Walgreens Boots. The stock is under review as our conviction in the name is decreasing. During the period, we started new positions in Criteo, Wabtec, Celgene, Iberdrola, Tencent, Howden and WPP.

Criteo provides web advertising services and offers a range of solutions such as click per cost and online banner displays. We believe Criteo is well positioned to benefit from the shift in display ads toward Real-Time Bidding (RTB) and programmatic buying in general, as we believe the company has strong technology and scale advantages.

Wabtec is the North America’s largest manufacturer of air brake systems and other products for the railroad and mass transit markets. The company’s brake products command a 50% market share in North America and its other products generally hold

the number 1 or number 2 position in their respective markets. Wabtec is a beneficiary of railroad operators’ spending to enhance productivity, growth in mass transit programmes globally and a potential pick up in infrastructure spending in the US. The company’s multipronged growth strategy includes introducing new products, enhancing international sales, expanding aftermarket exposure and acquiring bolt-on businesses.

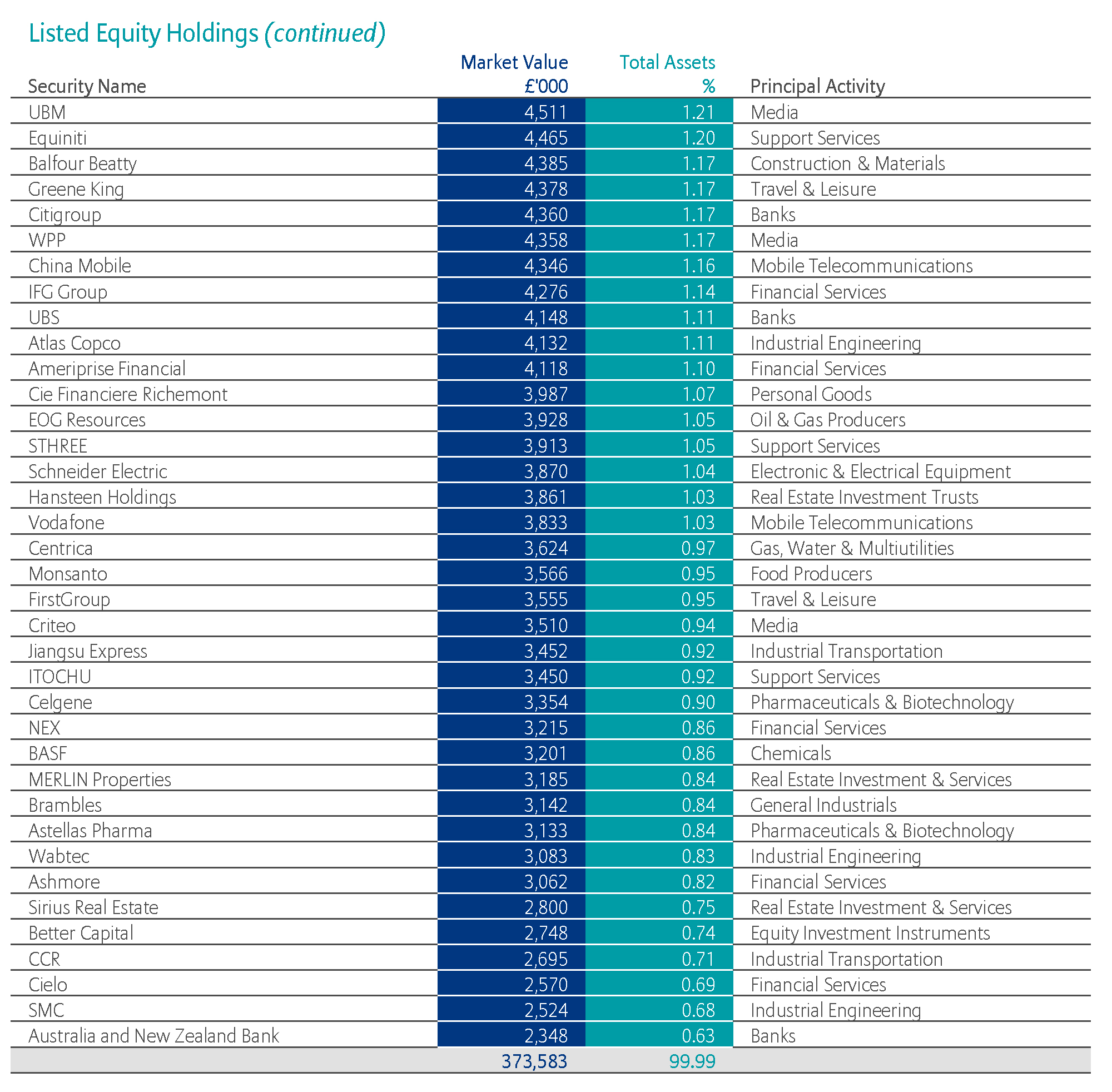

Sales included Total, BHP, Aviva, TGS, Flowserve, BT and ING Groep.

Flowserve continues to face pricing pressures due to reduced energy project activity and very competitive bidding from competitors. Industry fundamentals are likely to remain challenging and against this backdrop we have reinvested the proceeds in higher conviction stocks like Wabtec.

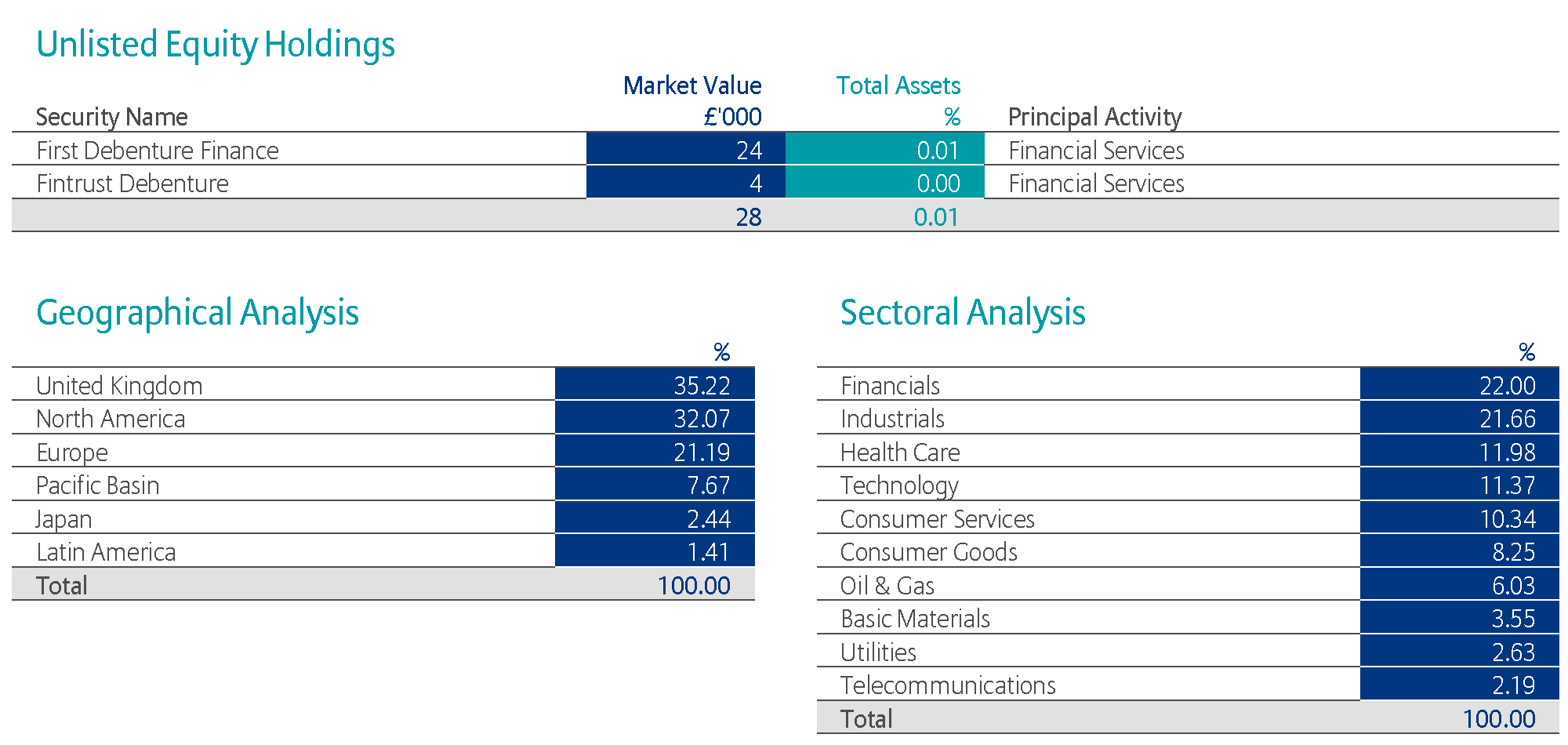

The benchmark for investing changed to 70 per cent global equities, represented by the FTSE World Ex UK Index, and 30 per cent UK equities, as represented by the FTSE All-Share Index, with effect from the AGM in March this year, the benchmark having previously been a 50:50 per cent split of the same indices. The portfolio manager had (and continues to have) considerable discretion either side of the benchmark proportions and had been investing increasingly in global equities, partly to diversify the income stream further, and partly to invest in attractive overseas growth opportunities. The revision to the benchmark reflects this of investing a higher proportion in global equities. The impact of the change in the benchmark has therefore been a gradual change to the investment strategy and stock selection. Over the reporting period, the change in benchmark has therefore had little impact on performance.

Expectations of a continued economic upswing and the still generous monetary policy of the leading international central banks should be positive for equities. Moreover, the good momentum of analysts’ corporate earnings estimates is also a good signal for the stock markets. At the same time, divergent monetary policies in the US and Europe and persistent political uncertainties might result in elevated volatility.

In this environment, active management is required to augment returns. We are comfortable taking advantage of these opportunities to buy high quality growth franchises at attractive valuations.

Lucy Macdonald Allianz Global Investors

This is no recommendation or solicitation to buy or sell any particular security. Any security mentioned above will not necessarily be comprised in the portfolio by the time this document is disclosed or at any other subsequent date. Investment trusts are quoted companies listed on the London Stock Exchange. Their share prices are determined by factors including the balance of supply and demand in the market, which means that the shares may trade below (at a discount to) or above (at a premium to) the underlying net asset value.

The Trust seeks to enhance returns for its shareholders through gearing in the form of long-term debentures. Gearing can boost the Trust’s returns when investments perform well, though losses can be magnified when investments lose value. You should be aware that this Trust may be subject to sudden and large falls in value and you could suffer substantial capital loss.

A trust’s Net Asset Value (NAV) is calculated as available shareholders’ funds divided by the number of shares in issue, with shareholders’ funds taken to be the net value of all the company’s assets after deducting liabilities. In line with current industry best practice NAVs are now shown that take into account the ‘fair value’ of debt. This means NAVs are calculated after allowing for the valuation of debt at fair value or current market price, rather than at final repayment value. NAVs with debt at market value provide a more realistic impact of the cost of debt, and thus a more realistic discount. It is the capital NAV that is shown, which excludes any income.

Investing involves risk. The value of an investment and the income from it may fall as well as rise and investors may not get back the full amount invested. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer and/or its affiliated companies at the time of publication. The data used is derived from various sources, and assumed to be correct and reliable, but it has not been independently verified; its accuracy or completeness is not guaranteed and no liability is assumed for any direct or consequential losses arising from its use, unless caused by gross negligence or wilful misconduct.

The conditions of any underlying offer or contract that may have been, or will be, made or concluded, shall prevail. Past performance is not a reliable indicator of future results.

The Trust is a UK public limited company traded openly on the stock market. A ranking, a rating or an award provides no indicator of future perforamcne and is not constant over time. You can purchase shares through a stock broker. Shares in the Trust can be held within an ISA and/or savings scheme and a number of providers offer this facility. A list of suppliers is available on our website.

This is a marketing communication issued by Allianz Global Investors GmbH, an investment company with limited liability, incorporated in Germany, with its registered office at Bockenheimer Landstrasse 42-44, D-60323 Frankfurt/Main, registered with the local court Frankfurt/Main under HRB 9340, authorised by Bundesanstalt für Finanzdienstleistungsaufsicht (www.bafin.de). Allianz Global Investors GmbH has established a branch in the United Kingdom, Allianz Global Investors GmbH, UK branch, which is subject to limited regulation by the Financial Conduct Authority (www.fca.org.uk).

Details about the extent of our regulation by the Financial Conduct Authority are available from us on request.

All data source Allianz Global Investors as at 31 December 2016 unless otherwise stated. Allianz Global Investors GmbH, UK Branch, 199 Bishopsgate, London EC2M 3TY