In a zero-interest-rate environment, market volatility has been driven up in the wake of new waves of the pandemic and rising geopolitical tensions. On the path toward an income-seeking portfolio, what are the strategies to capture higher potential income at measured risk?

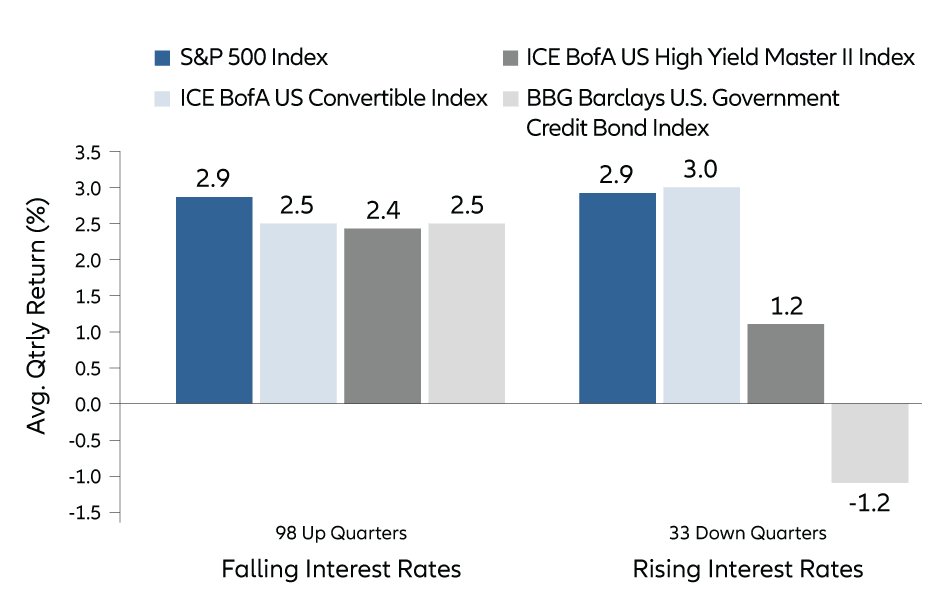

Is there a magic formula that ensures investors receive stable income throughout the boom and bust of an economic cycle? Each of the asset classes has distinctive features that contribute to varying performance under varied market conditions. To safely navigate market swings, investors should flexibly switch between these asset classes to optimise their full potentials.

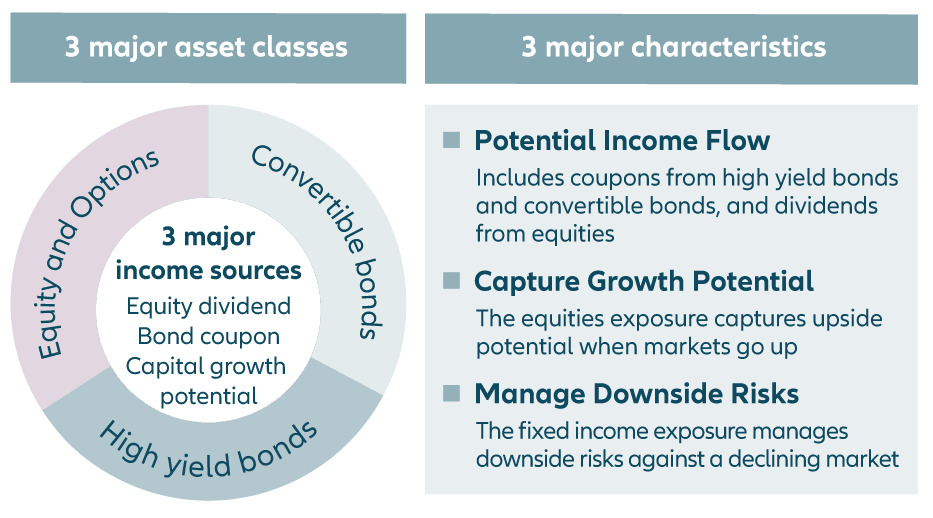

The AllianzGI Income and Growth strategy adopts a three-sleeve approach with asset classes of on equities, convertible bonds and high-yield bonds. This is an offensive yet defensive strategy approach that aims to capture the market’s upside potential while mitigating downside risks in a market downturn.

To accommodate investors’ needs, the fund offers multiple currency classes to allow investors the choice of investing into their base currency of investment, and adjusting their strategy according to market trends, including a risk factor of foreign exchange fluctuations.

Source: AllianzGI, as of September 2020. There is no guarantee that these investment strategies and processes will be effective under all market conditions and investors should evaluate their ability to invest for a long-term based on their individual risk profile especially during periods of downturn in the market.

Source: FactSet, ICE Data Services, BofA. Data as of 1 January 1988 to 30 September 2020. Past performance, or any prediction, projection or forecast, is not indicative of future performance. The actual future events may differ from the projections.

It has been almost a year since the coronavirus outbreak began. Despite news of vaccine rollouts, it is unclear when the world’s population will reach herd immunity. The lingering fear of recurring outbreaks is exacerbated by the US post-election uncertainty. Under such a foggy outlook, a resilient asset allocation that balances risk and return has become ever more important. A strategy aiming at consistent dividend distribution, capturing capital growth potential and managing downside risks may be one of the all-inclusive solutions to navigating through the market’s boom and bust.

For example, as the global bond yield nosedives, this strategy leverages US high-yield bonds for enhanced income, and invests in equities to capture growth potential. Meanwhile, this strategy takes advantage of convertible bonds’ combined features of stocks and bonds, capturing the equity market’s growth potential, while mitigating possible downside risks.

Allianz US Short Duration High Income Bond

Note: Dividend payments may, at the sole discretion of the Investment Manager, be made out of the Fund’s capital or effectively out of the Fund’s capital which represents a return or withdrawal of part of the amount investors originally invested and/or capital gains attributable to the original investment. This may result in an immediate decrease in the NAV per share and the capital of the Fund available for investment in the future and capital growth may be reduced, in particular for hedged share classes for which the distribution amount and NAV of any hedged share classes (HSC) may be adversely affected by differences in the interests rates of the reference currency of the HSC and the base currency of the Fund.

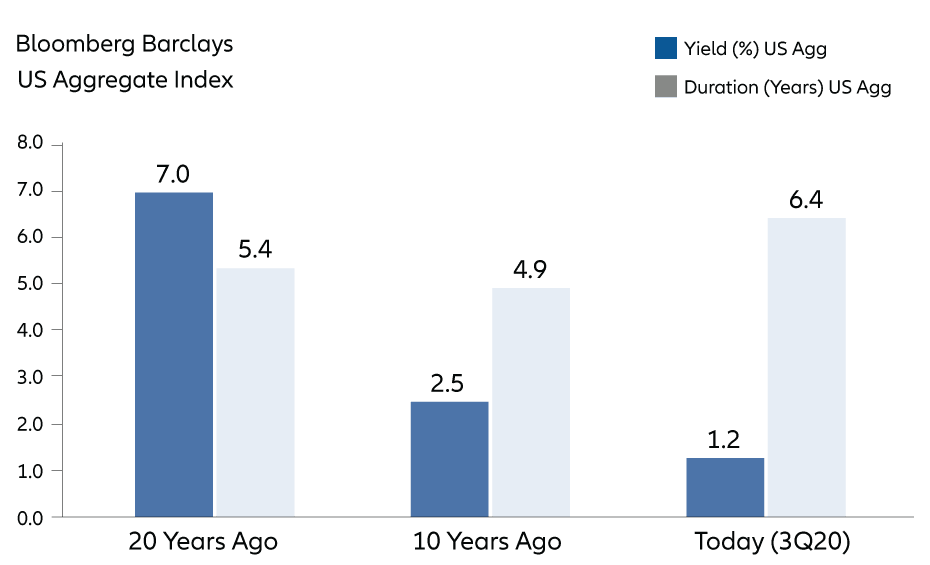

To boost slowing economies, the US Federal Reserve (the “US Fed”) and other central banks have enacted unprecedented expansionary monetary policies, pushing the world’s policy rates and bonds yield down close to zero, or even into the negative territory. Traditional core bonds no longer deliver reliable returns, as in the past, but, rather, heighten risk associated with their long durations.

Source: FactSet. Data as of 30 September 2020. Past performance, or any prediction, projection or forecast, is not indicative of future performance.

In contrast, US high-yield bonds maintain yield and spread advantage. With the US Fed and the US Government having adopted unconventional measures, multiple figures suggest that the high-yield market has recovered and is functioning normally. It provides an attractive buy-on-dip opportunity for long-term investors.

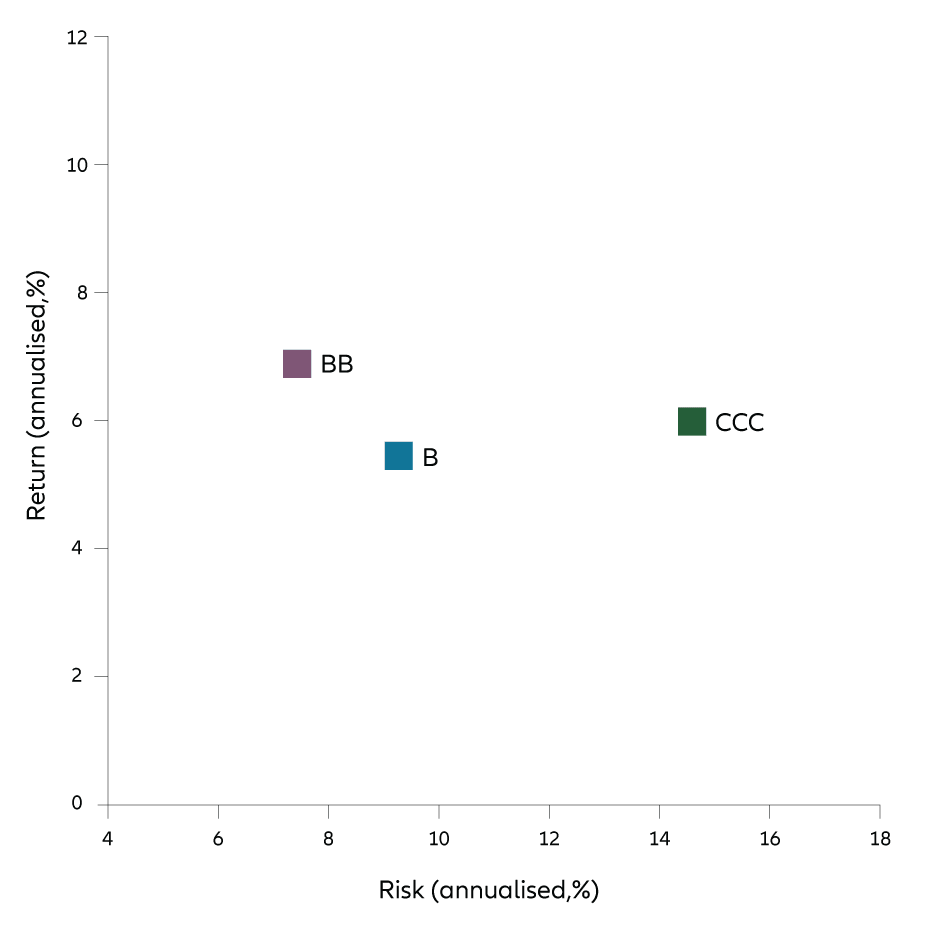

Amidst the cloudy economic outlook, investors anticipate increased defaults among high-yield issuers. Specifically, energy issuers are under the spotlight due to the plummet in oil prices earlier in 2020. However, the risk is largely concentrated on the most distressed credits within the exploration and production and oil field equipment and services sub-industries. Overall, the US high-yield bond market is well diversified across many industries. Individual credit defaults will unlikely affect the entire asset class.

As market volatilities persist, a portfolio with good quality bonds tends to provide better risk-adjusted returns. The Allianz US Short Duration High Income Bond fund currently focuses on good-quality high yield credits, believes lower-than-market volatility and default risk that balance risk and returns for investors.

Duration is a major indicator of bonds subject to interest rate risk. The longer the duration is, the more price-sensitive it is to interest rate changes. Accordingly, this fund targets shorter duration bonds to enhance the defensiveness of the portfolio.

Source: ICE Data Services, as at 30 September 2020. BB: ICE BofA BB US High Yield Index; B: ICE BofA B US High Yield Index; CCC: ICE BofA CCC and Lower US High Yield Index. Past performance, or any prediction, projection or forecast, is not indicative of future performance.

Allianz American Income

The Fund aims at long-term capital growth and income by investing in debt securities of American bond markets with a focus on the US bond markets.

The Fund is exposed to significant risks of investment/general market, country, emerging market, creditworthiness/credit rating, default, interest rate, volatility and liquidity, counterparty, valuation, sovereign debt and currency.

The Fund is also exposed to risks relating to securities lending transactions, repurchase agreements and reverse repurchase agreements.

The Fund may invest in high-yield (non-investment grade and unrated) investments and convertible bonds which may subject to higher risks, such as volatility, loss of principal and interest, creditworthiness and downgrading, default, interest rate, general market and liquidity risks. Convertibles will be exposed to prepayment risk, equity movement and greater volatility than straight bond investments. All these factors may adversely impact the net asset value of the Fund.

The Fund may invest in financial derivative instruments ("FDI") which may expose to higher leverage, counterparty, liquidity, valuation, volatility, market and over the counter transaction risks. The Fund’s net derivative exposure may be up to 50% of the Fund’s net asset value.

This investment may involve risks that could result in loss of part or entire amount of investors’ investment.

In making investment decisions, investors should not rely solely on this material.

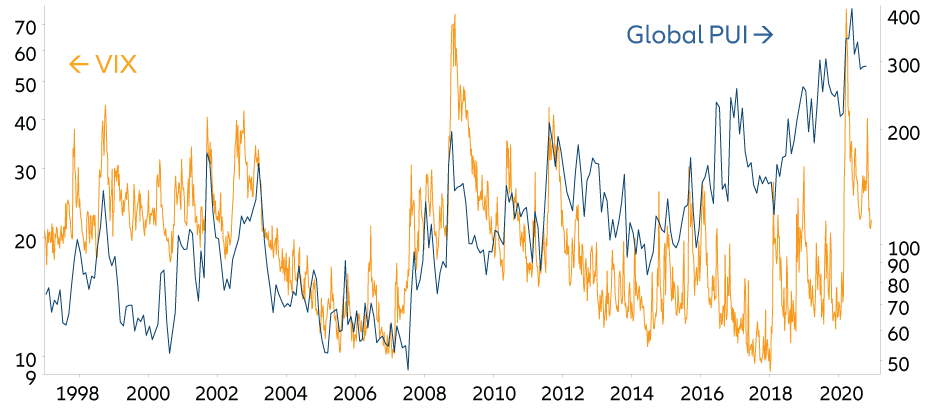

The speed and scale of the monetary and fiscal policy measures related to the pandemic have helped reduce the depth and longevity of the global recession, and the global economy has started to recover. Although the worst of the recession is behind us, returning to the pre-coronavirus growth trajectory may still take years. New vaccines appear to hold promise, but we still need to watch the key macroeconomic data points for signs of momentum – and we expect wide differences in how regions perform.

While the path of the economic recovery remains unclear, global political uncertainty is still high. New US Presidency and Congress, ongoing trade tensions (trade wars), geopolitics ( US vs China; Russia; North Korea; Iran etc.) need to closely monitor.

Source: AllianzGI, Refinitiv, Baker, Bloom, Davis; as of 14 December 2020.

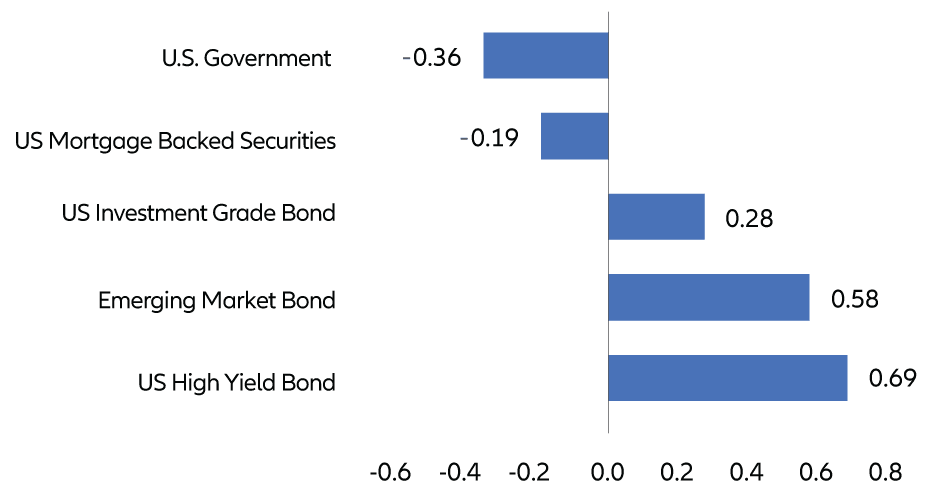

Given the massive amounts of monetary and fiscal stimulus, investors will feel side effects – high valuations in several major asset classes may cause volatility. Lowe correlation assets should help to balance your portfolio.

Source: AllianzGI, Blomberg, the correlation are bond indices versus S&P 500 index, US Government, US Mortgage Backed Securities, US Investment Grade Bond, Emerging Market Bond, US High Yield indices are refer to ICE Bofa Merrill Lynch indices; as of 30 November 2020.

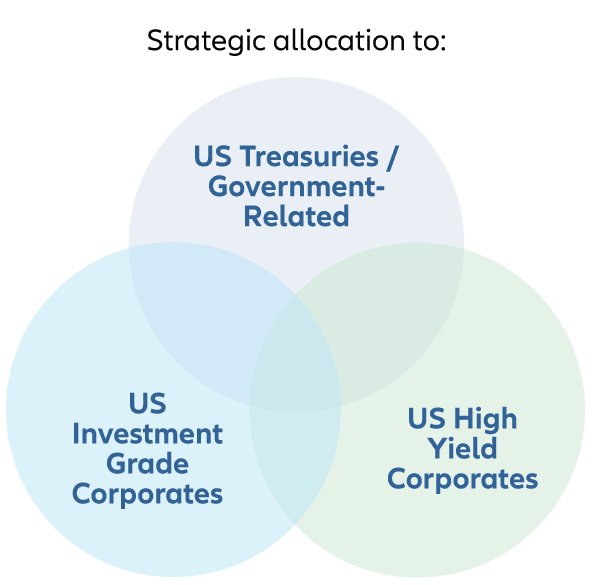

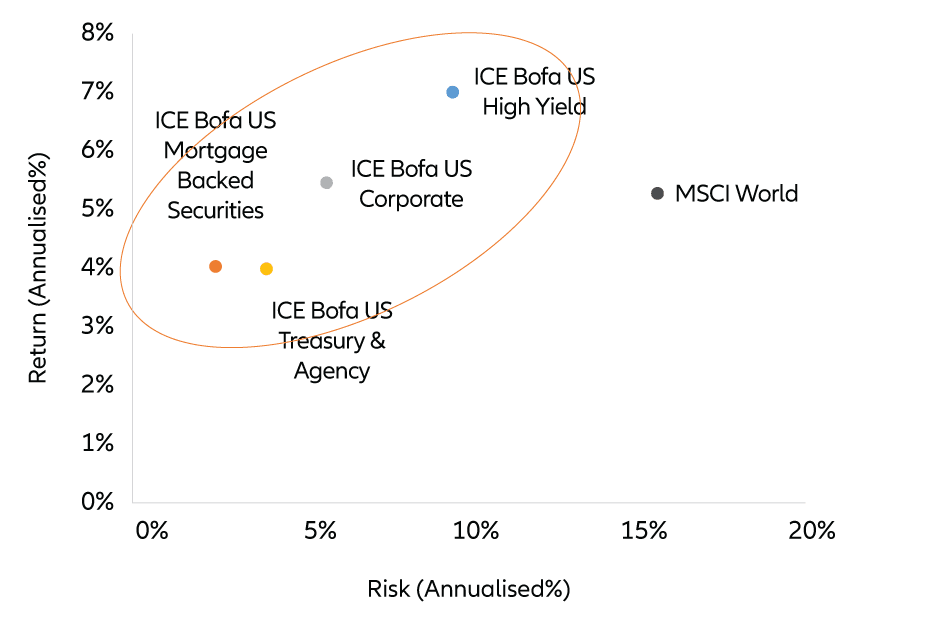

As uncertainty continues and most of equities valuation remain high, multi-fixed income assets could help to diversify the portfolio risks. The Allianz American Income fund is a blended fixed income strategy that aims to produce consistent and stable income while mitigating volatility and risk.

Source: AllianzGI, December 2020. There is no guarantee that these investment strategies and processes will be effective under all market conditions and investors should evaluate their ability to invest for a long-term based on their individual risk profile especially during periods of downturn in the market.

Source: AllianzGI, Blomberg; as of January 2005 to November 2020. Past performance, or any prediction, projection or forecast, is not indicative of future performance.